The Impact of Digital Financial Inclusion on Household Commercial Insurance for Sustainable Governance Mechanisms under Regional Group Differences

Abstract

:1. Introduction

2. Literature Review

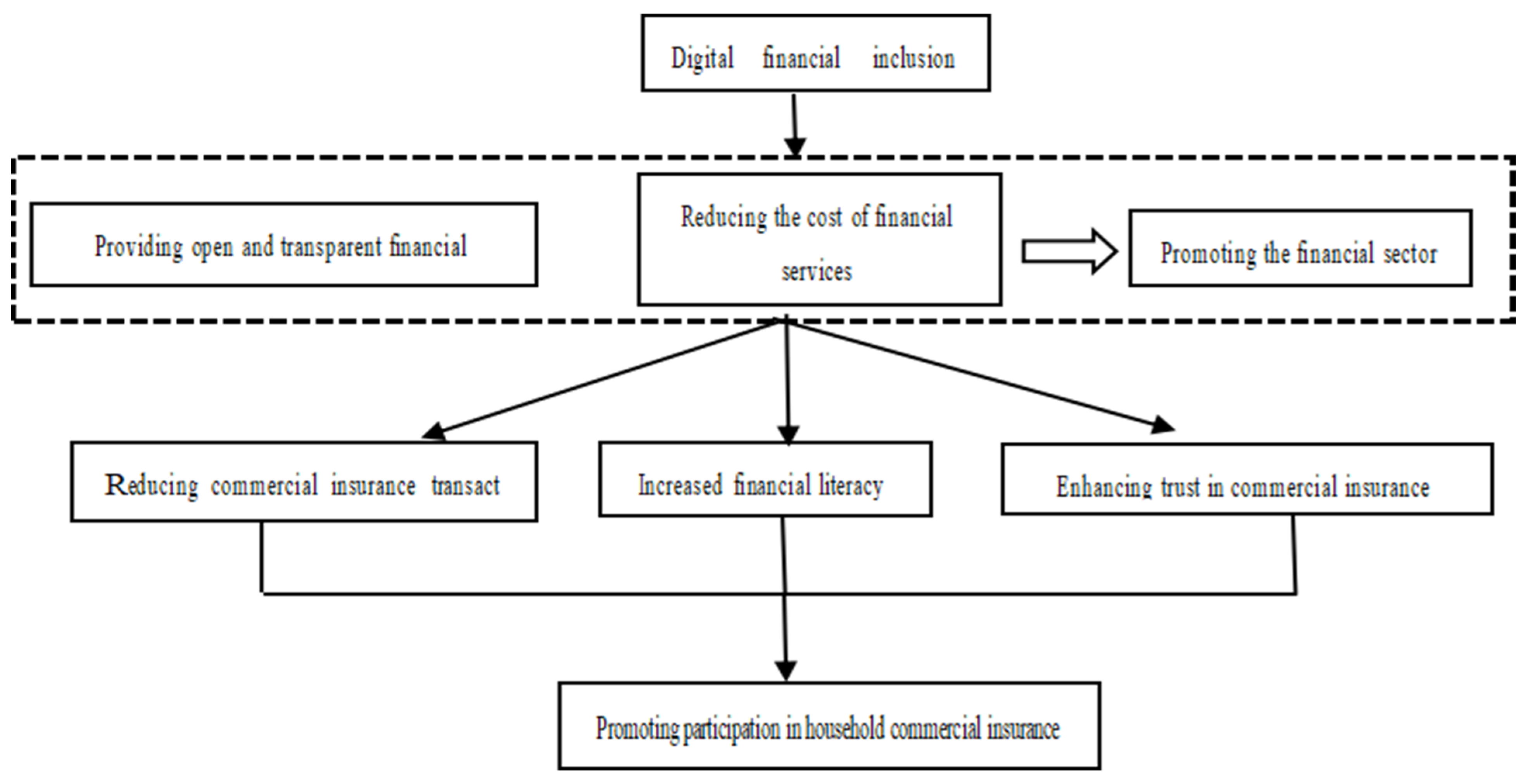

3. Theory and Mechanism Analysis

4. Model Construction and Data Sources

Data Sources

- (1)

- Core explained or outcome variables: the research objective of this paper is to examine the impact of the development of digital financial inclusion on commercial insurance; so, whether households participate in commercial insurance (Cin) is used as an explained variable. In the CFPS 2018 questionnaire, when the household’s commercial insurance expenditure in the past 12 months is greater than 0, it is regarded as participating in commercial insurance and assigned a value of 1. When the household’s commercial insurance expenditure in the past 12 months is equal to 0, it is regarded as not participating in commercial insurance and assigned a value of 0.

- (2)

- Core explanatory or independent variables: the research object of this paper is digital inclusive finance; the Peking University Digital Financial Inclusion Index provides a good measure, and the data are authoritative and reliable and can accurately reflect the recent development of China’s inclusive finance. In order to attenuate the endogeneity problem caused by reverse causality, this study divides China’s 2017 Digital Financial Inclusion Index (DFIIC) by 100 and lags it by one year to obtain the Digital Financial Inclusion Development variable (DFIIC), which is used as the core independent variable (the 2018 Chinese Family Panel Studies data correspond to the financial inclusion development variable as the 2017 Digital Financial Inclusion Index divided by 100).

- (3)

- Control variables: observable individual-, household-, and region-level characteristics all have an impact on commercial insurance participation. Individual-level control variables include age, gender, years of education, marital status, health, risk perception, party membership, relationship, social security, and private lending. The control variables at the household level include household size, log value of total household expenditure, log value of total household income, log value of the current year’s asset value of the house, and the proportion of favor spending in total expenditure; the control variables at the regional level include the per capita net income of the district and county in which the household is located (Ln pci), as well as the province, area, etc. The specific variables and assigned values are shown in Table 2.

5. Empirical Results and Their Implications

5.1. Methodology

5.2. Benchmark Regression

5.3. Endogeneity Test

5.4. Heterogeneity Test

5.5. Robustness Test

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Xie, Y.; Zhang, B.; Yao, Y.; Chen, X.; Wang, X. Mechanism of Human Capital Influence on Household Commercial Insurance Holding Behavior—An Empirical Analysis Based on China Household Finance Survey (CHFS) Data. Front. Environ. Sci. 2022, 10, 961184. [Google Scholar] [CrossRef]

- Yan, X.; Chen, H.; Yang, L.; Rao, K. Commercial Health Insurance under the New Healthcare Reform: Status, Problems and Strategies. Chin. J. Health Policy 2013, 6, 50–54. [Google Scholar]

- Zhang, T.; Li, W.; Li, K.; Liu, Z. Only Words Matter? The Effects of Cognitive Abilities on Commercial Insurance Participation. N. Am. J. Econ. Financ. 2022, 61, 101691. [Google Scholar] [CrossRef]

- Xu, B.-C.; Xu, X.-N.; Zhao, J.-C.; Zhang, M. Influence of Internet Use on Commercial Health Insurance of Chinese Residents. Front. Public Health 2022, 10, 907124. [Google Scholar] [CrossRef] [PubMed]

- Praveenkumar, S. An Empirical Analysis in the Critical Factors Influencing the Health Insurance Business in Achieving Sustainable Development Using Structural Equation Model. Int. Dev. Plan. Rev. 2023, 22, 95–109. [Google Scholar]

- Sun, D.; Chen, W.; Dou, X. Formation Mechanism of Residents’ Intention to Purchase Commercial Health Insurance: The Moderating Effect of Environmental Pollution Perception. J. Public Health 2023, 1–14. [Google Scholar] [CrossRef]

- Yogo, M. Portfolio Choice in Retirement: Health Risk and the Demand for Annuities, Housing, and Risky Assets. J. Monet. Econ. 2016, 80, 17–34. [Google Scholar] [CrossRef] [PubMed]

- Xu, N.; Zhao, R.; Li, Y. Credit Cards and Commercial Insurance Participation: Evidence from Urban Households in China. Account. Financ. 2024, 64, 1159–1182. [Google Scholar] [CrossRef]

- Guven, C.; Hoxha, I. Rain or Shine: Happiness and Risk-Taking. Q. Rev. Econ. Financ. 2015, 57, 1–10. [Google Scholar] [CrossRef]

- Showers, V.E.; Shotick, J.A. The Effects of Household Characteristics on Demand for Insurance: A Tobit Analysis. J. Risk Insur. 1994, 61, 492–502. [Google Scholar] [CrossRef]

- Choi, W.I.; Shi, H.; Bian, Y.; Hu, H. Development of Commercial Health Insurance in China: A Systematic Literature Review. BioMed Res. Int. 2018, 2018, 3163746. [Google Scholar] [CrossRef] [PubMed]

- Roussou, I.; Stiakakis, E.; Sifaleras, A. An Empirical Study on the Commercial Adoption of Digital Currencies. Inf. Syst. E-Bus. Manag. 2019, 17, 223–259. [Google Scholar] [CrossRef]

- Trivedi, S. Blockchain Framework for Insurance Industry. Int. J. Innov. Technol. Manag. 2023, 20, 2350034. [Google Scholar] [CrossRef]

- The Influence of Income Growth on the Premium Income of Commercial Endowment Insurance under the Aging Background. Available online: https://webofscience.clarivate.cn/wos/alldb/full-record/WOS:000519108000053 (accessed on 11 March 2024).

- Ren, T.; Zhao, Q.; Wang, W.; Ding, X. Air Pollution, Residents’ Concern and Commercial Health Insurance’s Sustainable Development. Front. Environ. Sci. 2023, 11, 1136274. [Google Scholar] [CrossRef]

- Chang, T.Y.; Huang, W.; Wang, Y. Something in the Air: Pollution and the Demand for Health Insurance. Rev. Econ. Stud. 2018, 85, 1609–1634. [Google Scholar] [CrossRef]

- Hu, X.; Wang, Z.; Liu, J. The Impact of Digital Finance on Household Insurance Purchases: Evidence from Micro Data in China. Geneva Pap. Risk Insur. Issues Pract. 2022, 47, 538–568. [Google Scholar] [CrossRef]

- Li, G.; Li, Z.; Lv, X. The Ageing Population, Dependency Burdens and Household Commercial Insurance Purchase: Evidence from China. Appl. Econ. Lett. 2021, 28, 294–298. [Google Scholar] [CrossRef]

- Si, W. P Ublic Health Insurance and the Labor Market: Evidence from China’s Urban Resident Basic Medical Insurance. Health Econ. 2021, 30, 403–431. [Google Scholar] [CrossRef] [PubMed]

- Jagani, K.; Patra, S. Digital Participation through Mobile Internet Banking and Its Impact on Financial Inclusion: A Study of Jan Dhan Yojana. Int. J. Public Adm. Digit. Age 2017, 4, 51–61. [Google Scholar] [CrossRef]

- Baranauskas, G. Digital and Customizable Insurance: Empirical Findings and Validation of Behavioral Patterns, Influential Factors, and Decision-Making Framework of Baltic Insurance Consumers in Digital Platforms. In Intelligent Systems in Digital Transformation: Theory and Applications; Springer: Berlin/Heidelberg, Germany, 2022; pp. 397–426. [Google Scholar]

- Ayimah, J.C.; Kuada, J.; Ayimey, E.K. Digital Financial Service Adoption Decisions of Semi-Urban Ghanaian University Students—Implications for Enterprise Development and Job Creation. Afr. J. Econ. Manag. Stud. 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Study on the Impact of Digital Inclusive Finance on Rural Land Transfer and Its Mechanism: Empirical Evidence from CFPS and PKU-DFIIC. Available online: https://webofscience.clarivate.cn/wos/alldb/full-record/WOS:000905024100058 (accessed on 11 March 2024).

- Dai, M.; Cao, H. The Impact of Digital Finance on the Operating Performance of Commercial Banks: Promotion or Inhibition? In E-Business. Digital Empowerment for an Intelligent Future; Tu, Y., Chi, M., Eds.; Lecture Notes in Business Information Processing; Springer Nature: Cham, Switzerland, 2023; Volume 481, pp. 1–11. ISBN 978-3-031-32301-0. [Google Scholar]

- Johnen, C.; Mußhoff, O. Digital Credit and the Gender Gap in Financial Inclusion: Empirical Evidence from Kenya. J. Int. Dev. 2023, 35, 272–295. [Google Scholar] [CrossRef]

- Yue, P.; Korkmaz, A.G.; Yin, Z.; Zhou, H. The Rise of Digital Finance: Financial Inclusion or Debt Trap? Financ. Res. Lett. 2022, 47, 102604. [Google Scholar] [CrossRef]

- Han, H.; Hai, C.; Wu, T.; Zhou, N. How Does Digital Infrastructure Affect Residents’ Healthcare Expenditures? Evidence from Chinese Microdata. Front. Public Health 2023, 11, 1122718. [Google Scholar] [CrossRef] [PubMed]

- Kefeng, Y.; Xiaoxia, Z.; Nedospasova, O.P. The Impact of Digital Divide on Household Participation in Risky Financial Investments: Evidence From China. Chang. Soc. Pers. 2023, 7, 113. [Google Scholar] [CrossRef]

- Li, Y.; Long, H.; Ouyang, J. Digital Financial Inclusion, Spatial Spillover, and Household Consumption: Evidence from China. Complexity 2022, 2022, 8240806. [Google Scholar] [CrossRef]

- Jiang, W.; Hu, Y.; Cao, H. Does Digital Financial Inclusion Increase the Household Consumption? Evidence from China. J. Knowl. Econ. 2024, 125, 106377. [Google Scholar] [CrossRef]

- Hu, D.; Zhai, C.; Zhao, S. Does Digital Finance Promote Household Consumption Upgrading? An Analysis Based on Data from the China Family Panel Studies. Econ. Model. 2023, 125, 106377. [Google Scholar] [CrossRef]

- Shi, Y.; Cheng, Q.; Wu, Y.; Lin, Q.; Xu, A.; Zheng, Q. Promoting or Inhibiting? Digital Inclusive Finance and Cultural Consumption of Rural Residents. Sustainability 2023, 15, 2719. [Google Scholar] [CrossRef]

- Wang, X.; Mao, Z. Research on the Impact of Digital Inclusive Finance on the Financial Vulnerability of Aging Families. Risks 2023, 11, 209. [Google Scholar] [CrossRef]

- Xie, X. Analyzing the Impact of Digital Inclusive Finance on Poverty Reduction: A Study Based on System GMM in China. Sustainability 2023, 15, 13331. [Google Scholar] [CrossRef]

- Liu, L.; Guo, L. Digital Financial Inclusion, Income Inequality, and Vulnerability to Relative Poverty. Soc. Indic. Res. 2023, 170, 1155–1181. [Google Scholar] [CrossRef]

- Mushtaq, R.; Bruneau, C. Microfinance, Financial Inclusion and ICT: Implications for Poverty and Inequality. Technol. Soc. 2019, 59, 101154. [Google Scholar] [CrossRef]

- Skogh, G. The Transactions Cost Theory of Insurance—Contracting Impediments and Costs. J. Risk Insur. 1989, 56, 726. [Google Scholar] [CrossRef]

- Liu, Z.; Zhang, Y.; Li, H. Digital Inclusive Finance, Multidimensional Education, and Farmers’ Entrepreneurial Behavior. Math. Probl. Eng. 2021, 2021, 6541437. [Google Scholar] [CrossRef]

- Abhijith, P.S.; Joseph K., A. Reverse FinTech Socialisation: A Remedy for Financial Exclusion in the Digital Era. Int. J. E-Bus. Res. 2023, 18, 1–17. [Google Scholar] [CrossRef]

- Li, X.; Wu, Y.; Li, J. Digital Financial Development and Household Participation in Commercial Insurance. Stat. Res. 2021, 38, 29–41. (In Chinese) [Google Scholar] [CrossRef]

{kind=link}

| Province | The Digital Financial Inclusion Index | Province | The Digital Financial Inclusion Index | ||

|---|---|---|---|---|---|

| 2017 | Value/100 | 2017 | Value/100 | ||

| National average | 319.01 | 3.19 | Henan | 328.09 | 3.28 |

| Beijing | 326.02 | 3.26 | Hubei | 331.10 | 3.31 |

| Tianjin | 322.91 | 3.23 | Hunan | 318.96 | 3.19 |

| Hebei | 313.87 | 3.14 | Guangdong | 304.92 | 3.05 |

| Shanxi | 324.92 | 3.25 | Guangxi | 326.44 | 3.26 |

| Neimenggu | 340.10 | 3.4 | Hainan | 309.34 | 3.09 |

| Liaoning | 313.57 | 3.14 | Chongqing | 319.57 | 3.2 |

| Jilin | 310.72 | 3.11 | Sichuan | 325.14 | 3.25 |

| Heilongjiang | 323.77 | 3.24 | Guizhou | 316.99 | 3.17 |

| Shanghai | 330.31 | 3.3 | Yunnan | 316.08 | 3.16 |

| Jiangsu | 324.69 | 3.25 | Xizang | 314.10 | 3.14 |

| Zhejiang | 322.66 | 3.23 | Shanxi | 317.47 | 3.17 |

| Anhui | 324.48 | 3.24 | Gansu | 304.10 | 3.04 |

| Fujian | 314.47 | 3.14 | Qinghai | 301.42 | 3.01 |

| Jiangxi | 324.38 | 3.24 | Ningxia | 305.24 | 3.05 |

| Shandong | 319.92 | 3.2 | Xinjiang | 313.56 | 3.14 |

| Variables and Symbols | Assign a Value | Obs. | Mean | Min | Max | Std. Dev. |

|---|---|---|---|---|---|---|

| Commercial insurance participation (Cin) | Participation in commercial insurance, assigned a value of 1, otherwise 0 | 2644 | 0.357 | 0 | 1 | 0.479 |

| Financial inclusion index (DFIIC) | Digital Financial Inclusion Index 2017/100 | 2644 | 3.172 | 3.041 | 3.311 | 0.085 |

| Age | Age of head of household | 2644 | 47.51 | 19 | 82 | 9.087 |

| Gender | Male heads of household are assigned a value of 1 and females are assigned a value of 0 | 2644 | 0.493 | 0 | 1 | 0.500 |

| Educational attainment (Edu) | Years of education of the head of household | 2644 | 7.449 | 0 | 19 | 4.345 |

| Marital status (Marriage) | Head of household married is assigned a value of 1 and other is assigned 0 | 2644 | 0.904 | 0 | 1 | 0.294 |

| Health status (Health) | A self-assessed health score of 6 and above is considered healthy and assigned a value of 1, while a score of 5 and below is considered unhealthy and assigned a value of 0 | 2644 | 0.807 | 0 | 1 | 0.394 |

| Risk appetite (Risk) | A risk value of 6 and above is considered as risk appetite and assigned a value of 1, while a score of 5 and below is considered as risk aversion and assigned a value of 0 | 2644 | 0.204 | 0 | 1 | 0.403 |

| Political party member (Party) | The head of the household is a member of the party assigned the value 1 and others are assigned a value of 0 | 2644 | 0.008 | 0 | 1 | 0.087 |

| Interpersonal relationship (Relation) | An interpersonal score of 6 and above is considered a good interpersonal relationship and assigned a value of 1, while a score of 5 and below is considered a bad interpersonal relationship and assigned a value of 0 | 2644 | 0.715 | 0 | 1 | 0.451 |

| Social security (Sin) | Having social security is assigned a value of 1, otherwise it is assigned a value of 0 | 2644 | 0.957 | 0 | 1 | 0.204 |

| Private loan (Ple) | Have private lending assigned a value of 1, otherwise assigned a value of 0 | 2644 | 0.164 | 0 | 1 | 0.370 |

| Family size (Size) | Number of persons in the household | 2644 | 3.962 | 1 | 14 | 1.693 |

| Household expenditures (Ln exp) | Total annual household expenditure in logarithmic terms | 2644 | 10.84 | 6.820 | 18.42 | 0.857 |

| Household income (Ln inc) | Gross annual household income in logarithms | 2631 | 10.58 | 2.303 | 13.53 | 0.954 |

| Housing value (Ln house) | The current year’s value of the house is taken as a logarithm | 2644 | 11.88 | 5.704 | 17.50 | 1.333 |

| Expenditure on favours/total expenditure (Exp) | Expenditures incurred during interpersonal interactions throughout the year aimed at maintaining social relationships (such as gifts, holiday greetings, etc.), expressed as a percentage of total expenditures for the year | 2644 | 0.083 | 0 | 0.749 | 0.089 |

| District net income per capital (Ln pci) | District and county net income per capital in logarithmic terms | 2643 | 9.872 | 7.419 | 11.93 | 0.476 |

| Province | Eastern region assigned value 1, central region 2, western region 3 | 2644 | 1.897 | 1 | 3 | 0.833 |

| Area | Urban is assigned a value of 1 and rural is 0 | 2644 | 0.426 | 0 | 1 | 0.495 |

| Explained Variable: Cin | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Probit 1 | Probit 2 | Probit 3 | Probit 4 | |

| DFIIC | 1.910 *** | 1.581 *** | 1.099 *** | 1.046 *** |

| (6.45) | (5.13) | (3.41) | (3.22) | |

| Age | −0.019 *** | −0.010 *** | −0.011 *** | |

| (−6.08) | (−2.96) | (−3.17) | ||

| Gender | −0.062 | −0.045 | −0.040 | |

| (−1.16) | (−0.79) | (−0.70) | ||

| Edu | 0.062 *** | 0.029 *** | 0.027 *** | |

| (9.19) | (3.81) | (3.55) | ||

| Marriage | 0.437 *** | 0.192 | 0.205 * | |

| (4.19) | (1.57) | (1.67) | ||

| Health | 0.166 ** | 0.063 | 0.061 | |

| (2.38) | (0.86) | (0.83) | ||

| Risk | −0.012 | −0.086 | −0.087 | |

| (−0.18) | (−1.24) | (−1.25) | ||

| Party | 0.197 | 0.131 | 0.131 | |

| (0.67) | (0.41) | (0.40) | ||

| Relation | 0.145 ** | 0.054 | 0.055 | |

| (2.47) | (0.87) | (0.88) | ||

| Sin | 0.386 *** | 0.390 *** | 0.410 *** | |

| (2.76) | (2.65) | (2.76) | ||

| Size | −0.017 | −0.008 | ||

| (−0.99) | (−0.46) | |||

| Ple | 0.105 | 0.109 | ||

| (1.37) | (1.42) | |||

| Ln inc | 0.238 *** | 0.224 *** | ||

| (4.07) | (3.85) | |||

| Ln exp | 0.488 *** | 0.476 *** | ||

| (6.52) | (6.37) | |||

| Ln house | 0.041 | 0.030 | ||

| (1.47) | (1.11) | |||

| Exp | −0.872 ** | −0.886 ** | ||

| (−2.27) | (−2.32) | |||

| Ln pci | 0.133 * | |||

| (1.86) | ||||

| Constant term | −6.430 *** | −5.956 *** | −12.461 *** | −13.222 *** |

| (−6.83) | (−5.99) | (−10.22) | (−10.45) | |

| Pseudo R2 | 0.012 | 0.085 | 0.194 | 0.195 |

| Obs | 2644 | 2644 | 2631 | 2630 |

| Variable Name | (1) | (2) |

|---|---|---|

| Probit | Probit | |

| DFIIC | 0.260 * | 0.753 *** |

| (1.71) | (4.43) | |

| Control variable | N | Y |

| Constant term | −1.221 ** | −13.099 *** |

| (−2.44) | (−12.48) | |

| Pseudo R2 | 0.001 | 0.197 |

| Obs | 2644 | 2630 |

| Variable Name | Urban and Rural Subgroups | Area Grouping | Risk Perception Subgroup | ||||

|---|---|---|---|---|---|---|---|

| Countryside | City | East | Central | West | Risk Appetite | Risk Aversion | |

| DFIIC | 1.353 *** | 0.954 * | 1.335 ** | −0.156 | 1.973 *** | 2.583 *** | 0.698 * |

| (2.97) | (1.88) | (2.03) | (−0.14) | (2.85) | (3.41) | (1.86) | |

| Age | −0.014 *** | −0.007 | −0.014 *** | −0.003 | −0.012 * | −0.007 | −0.012 *** |

| (−3.03) | (−1.33) | (−2.64) | (−0.41) | (−1.73) | (−0.97) | (−2.95) | |

| Gender | −0.027 | −0.086 | −0.164 * | −0.071 | 0.148 | 0.138 | −0.098 |

| (−0.34) | (−1.03) | (−1.83) | (−0.67) | (1.32) | (1.12) | (−1.53) | |

| Edu | 0.033 *** | 0.030 ** | 0.038 *** | 0.025 * | 0.022 * | 0.030 * | 0.026 *** |

| (3.21) | (2.44) | (2.65) | (1.73) | (1.67) | (1.80) | (2.97) | |

| Marriage | 0.016 | 0.422 *** | 0.159 | 0.188 | 0.326 | 0.045 | 0.264 ** |

| (0.11) | (2.59) | (0.94) | (0.85) | (1.62) | (0.20) | (2.08) | |

| Health | 0.060 | 0.052 | 0.193 | 0.064 | 0.004 | 0.079 | 0.052 |

| (0.61) | (0.44) | (1.54) | (0.46) | (0.03) | (0.48) | (0.61) | |

| Party | 0.636 | −0.103 | −0.359 | 1.056 | 0.578 | 0.262 | 0.172 |

| (1.24) | (−0.26) | (−0.82) | (1.43) | (0.99) | (0.48) | (0.46) | |

| Relation | 0.073 | 0.019 | 0.128 | 0.146 | −0.134 | −0.031 | 0.070 |

| (0.85) | (0.21) | (1.33) | (1.20) | (−1.12) | (−0.22) | (0.99) | |

| Sin | 0.324 | 0.446 ** | 0.523 *** | 0.003 | 0.728 | 0.613 ** | 0.316 * |

| (1.51) | (2.18) | (2.61) | (0.01) | (1.59) | (2.14) | (1.82) | |

| Size | −0.007 | −0.030 | 0.001 | −0.020 | −0.031 | −0.020 | −0.007 |

| (−0.30) | (−1.02) | (0.05) | (−0.58) | (−0.90) | (−0.48) | (−0.36) | |

| Ple | −0.008 | 0.290 ** | 0.061 | 0.374 *** | −0.023 | 0.217 | 0.081 |

| (−0.08) | (2.26) | (0.43) | (2.61) | (−0.18) | (1.35) | (0.93) | |

| Ln inc | 0.158 *** | 0.347 *** | 0.238 *** | 0.468 *** | 0.105 | 0.059 | 0.284 *** |

| (3.13) | (4.95) | (3.27) | (5.48) | (1.64) | (0.75) | (5.81) | |

| Ln exp | 0.652 *** | 0.307 *** | 0.327 *** | 0.512 *** | 0.629 *** | 0.345 *** | 0.513 *** |

| (10.21) | (4.88) | (4.69) | (6.26) | (7.33) | (4.11) | (9.88) | |

| Ln house | 0.065 * | 0.017 | 0.035 | 0.113 ** | −0.018 | 0.149 *** | −0.010 |

| (1.74) | (0.43) | (0.82) | (2.24) | (−0.38) | (2.58) | (−0.34) | |

| Exp | −0.705 | −1.261 ** | −1.082 ** | −0.366 | −1.729 ** | −1.204 | −0.912 ** |

| (−1.58) | (−2.02) | (−2.09) | (−0.52) | (−2.16) | (−1.41) | (−2.30) | |

| Ln pci | 0.121 | 0.183 * | 0.084 | 0.096 | 0.290 * | 0.088 | 0.150 * |

| (1.19) | (1.80) | (0.82) | (0.65) | (1.87) | (0.60) | (1.88) | |

| Constant term | −15.300 *** | −13.034 *** | −12.294 *** | −13.087 *** | −17.543 *** | −16.179 *** | −12.738 *** |

| (−8.84) | (−7.12) | (−5.73) | (−3.35) | (−6.80) | (−6.18) | (−9.30) | |

| Pseudo R2 | 0.204 | 0.168 | 0.202 | 0.229 | 0.195 | 0.187 | 0.207 |

| Obs | 1507 | 1123 | 1061 | 779 | 790 | 537 | 2093 |

| Variable Name | (1) | (2) |

|---|---|---|

| Logit | Logit | |

| DFIIC | 3.104 *** | 1.873 *** |

| (6.41) | (3.41) | |

| Control variable | N | Y |

| Constant term | −10.443 *** | −23.227 *** |

| (−6.79) | (−10.77) | |

| Pseudo R2 | 0.012 | 0.199 |

| Obs | 2644 | 2630 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hou, Z.; Xu, J.; Choi, Y.; Ma, Y. The Impact of Digital Financial Inclusion on Household Commercial Insurance for Sustainable Governance Mechanisms under Regional Group Differences. Sustainability 2024, 16, 3596. https://0-doi-org.brum.beds.ac.uk/10.3390/su16093596

Hou Z, Xu J, Choi Y, Ma Y. The Impact of Digital Financial Inclusion on Household Commercial Insurance for Sustainable Governance Mechanisms under Regional Group Differences. Sustainability. 2024; 16(9):3596. https://0-doi-org.brum.beds.ac.uk/10.3390/su16093596

Chicago/Turabian StyleHou, Zaikun, Jing Xu, Yongrok Choi, and Yunning Ma. 2024. "The Impact of Digital Financial Inclusion on Household Commercial Insurance for Sustainable Governance Mechanisms under Regional Group Differences" Sustainability 16, no. 9: 3596. https://0-doi-org.brum.beds.ac.uk/10.3390/su16093596