Balancing Techniques for Advanced Financial Distress Detection Using Artificial Intelligence

Department of Applied Informatics, Vytautas Magnus University, Universiteto Street 10–202, 53361 Akademija, Lithuania

*

Author to whom correspondence should be addressed.

Electronics 2024, 13(8), 1596; https://0-doi-org.brum.beds.ac.uk/10.3390/electronics13081596

Submission received: 26 February 2024

/

Revised: 12 April 2024

/

Accepted: 18 April 2024

/

Published: 22 April 2024

(This article belongs to the Special Issue New Trends in Artificial Neural Networks and Its Applications)

Abstract

:Imbalanced datasets are one of the main issues encountered by artificial intelligence researchers, as machine learning (ML) algorithms can become biased toward the majority class and perform insufficiently on the minority classes. Financial distress (FD) is one of the numerous real-world applications of ML, struggling with this issue. Furthermore, the topic of financial distress holds considerable interest for both academics and practitioners due to the non-determined indicators of condition states. This research focuses on the involvement of balancing techniques according to different FD condition states. Moreover, this research was expanded by implementing ML models and dimensionality reduction techniques. During the course of this study, a Combined FD was constructed using five distinct conditions, ten distinct class balancing techniques, five distinct dimensionality reduction techniques, two features selection strategies, eleven machine learning models, and twelve weighted majority algorithms (WMAs). Results revealed that the highest area under the receiver operating characteristic (ROC) curve (AUC) score was achieved when using the extreme gradient boosting machine (XGBoost) feature selection technique, the experimental max number strategy, the undersampling methods, and the WMA 3.1 weighted majority algorithm (i.e., with categorical boosting (CatBoost), XGBoost, and random forest (RF) having equal voting weights). Moreover, this research has introduced a novel approach for setting the condition states of financial distress, including perspectives from debt and change in employment. These outcomes have been achieved utilizing authentic enterprise data from small and medium Lithuanian enterprises.

1. Introduction

Financial distress (FD) occurs when a business faces challenges from external economic conditions or internal financial decisions, leading to difficulties, such as inadequate cash flow, declining profitability, or the possibility of bankruptcy [1]. Researchers often focus on stock market enterprises due to the comprehensive and frequently accessible financial data they provide. However, small and medium-sized enterprises (SMEs) are often overlooked. SMEs have a substantial impact on the economy and employment. Nevertheless, SME financial reporting quality is generally low due to its private nature [2]. Despite being private entities, these enterprises are still subject to assessments of financial stability by banks, business partners, and government institutions. These stakeholders emphasize the need for more accurate and transparent financial reporting, ensuring a clearer understanding of an enterprise’s financial health. Regardless of data quality issues, the definition of financial distress state varies in different articles, from net income, or equity condition to financial ratio analysis (EBIT/interest expense, net loss/equity, etc.) or Altman Z-score categorization. The expansion of data and its increased accessibility presents opportunities for a more accurate identification and targeting of financial distress conditions. Notably, Altman’s research on financial distress, conducted in 1968, occurred during an era of limited data availability. As a result, Altman’s FD score is deemed more appropriate for publicly traded companies rather than SMEs. Consequently, there is a growing recognition of the need to broaden the criteria for assessing financial distress conditions. Therefore, to fill this gap, this research analyzes the different financial distress conditions and how well machine learning models perform in identifying them.

Moreover, the identification of financial distress features can help uncover underlying financial weaknesses or risks, contributing to more informed investor decision making, and aiding financial institutions in making lending decisions [3]. Moreover, the interdependencies among businesses and economic instability have the potential to trigger cascading effects on society and the overall economy [2]. Consequently, the government needs to engage in timely intervention, anticipating and effectively managing financial crises to ensure prompt and effective control. Furthermore, creating a model capable of gauging the probability of a company declaring bankruptcy holds significance for creditors, investors, regulators, and managers [4]. Additionally, the early warning signs can become an essential component in the decision making process [5]. The presumption of detecting early warning signs of financial distress is commonly found in research papers. However, challenges arise from the increasing availability of data, leading to complex feature interrelationships. Historical methods rely on ratios derived from financial statements, which are limited by delayed data. Nowadays, researchers aim to expand analysis by including additional features, leading to a high-dimensional feature space categorized as Big Data. Machine learning models become crucial for extracting meaningful patterns and developing accurate predictive models. However, including numerous features can lead to overfitting and reduced accuracy, highlighting the importance of identifying essential features for robust model development. Therefore, this study not only incorporates various feature selection techniques, but also proposes strategies for determining the size of features, which build upon the continuation of previous authors’ research.

Additionally, class distribution is commonly imbalanced. The percentage of financially stable enterprises is significantly higher than that of financial distress cases. Since traditional classification algorithms often give the majority class more weight to improve the overall model’s accuracy, the unequal distribution of the two classes will have a detrimental effect on the created financial distress detection models’ performance [4]. Financial distress class recognition is an essential task, which is usually ignored in this situation [1,4]. Therefore, for this research, one of the major focuses for this research was on the analysis of different class imbalance methods and their effectiveness. It is known that, to overcome the poor performance of the model, data level balancing techniques, e.g., oversampling, undersampling, or hybrid, are often used. Researchers frequently concentrate on eliminating undersampling techniques due to their insufficient ability to provide enough information and their inaccurate reflection of the proportion of companies facing bankruptcy in the actual business environment [6]. However, the main advantage of undersampling techniques is the elimination of redundant information. Therefore, it is important to include all different data-level approach techniques for the FD problem in the analysis. Additionally, this research introduces a novel proposal for deep neural networks, specifically the generative adversarial networks (GANs), to tackle the issue of class imbalance. Moreover, our objective is to demonstrate not only the efficiency of imbalance methods, but also the effectiveness of machine learning algorithms in identifying FD.

This research aims to provide insights regarding the impact of balancing techniques on the detection of financial distress. In addition, the definition of financial distress is expanded in novel condition states by incorporating debt and employment change states. The suggested framework employs feature selection techniques with different numbers of feature selection strategies, balancing techniques, and machine learning models. The five research questions that were analyzed in this research are as follows; RQ1: what is the difference between machine learning model performances for different financial distress conditions? RQ2: how does the use of different feature selection techniques affect the results? Do selected features have the same patterns? RQ3: which strategy is more effective for determining the size of features: an experimental or rule-based approach? RQ4: which method of class balancing is the most effective for identifying financial distress? RQ5: which machine learning model performs better in identifying financial distress? In total, 9428 experiments have been conducted. The data consisted of 64,648 Lithuanian SMEs (during the 2015–2022 period), wherein each enterprise was described by a feature space of 1020. During the ML experiments, the efficiency evaluation had been conducted using AUC, Gini, G-mean, and other metrics. The proposed methodology is transferable to all SMEs that provide annual reports and have available data regardless of legal status, debt, and employment changes.

The main research parts are organized as detailed further. Section 2 presents a literature analysis of financial distress condition states, used features, and balancing techniques. Section 3 provides with the description of Lithuanian SMEs’ data. Section 4 presents the proposed theoretical framework, whereas Section 5 provides a comparison of its obtained results. Section 6 and Section 7 discuss the results and give the main conclusion for this research.

2. Literature Analysis

2.1. Financial Distress Definition Determination and Features Analysis

Financial distress is a situation wherein an enterprise faces difficulties fulfilling its financial obligations [7,8]. However, there is no consensus on the definition of difficulties in fulfilling its financial obligations. Generally, the financial distress in an enterprise is an intermediate state that could lead to either recovery or bankruptcy [9]. The words failure and default are synonyms of bankruptcy [10,11], and bankruptcy is defined as the legal status of an enterprise when the enterprise cannot repay its debt and creditors take legal actions [7,10,12,13]. The bankruptcy classification system comprises two distinct categories, namely bankrupt and non-bankrupt, which entails the characterization of legal proceedings. Rather than financial distress, which depends on the researcher’s interpretation, an enterprise can be categorized into two classes (financially distressed or not) or three classes (healthy, financially distressed, bankrupt). In the Chinese stock market, ST (Special Treatment) labeling is used as a financial distress indicator. Companies that obtain such an ‘‘abnormal situation’’ label may be excluded from the stock market listing [14]. However, in other markets, researchers do not have such labeling. Therefore, different conditions are used as class identifiers, e.g., negative income or EBIT for 2–3 consecutive years, etc. All financial distress identification forms described in Table 1 can be used for stock companies. However, indicators that can only be used by small-medium enterprises (SMEs) are marked with ✓ in Table 1 due to lower requirements for the financial statement.

Additionally, the beginning of bankruptcy classification is associated with Beaver (1966) and Altman’s (1968) studies in the late 1960s [3,69]. In these studies, the viewpoint of financial indicators is that these indicators are the main historical information holders of the enterprise, for further classification analysis. The technical improvements and data availability led to the incorporation of additional features into financial distress analysis for better model classification and a more universal model creation [9]. However, in the models, the majority of features retain financial ratios due to financial information disclosures and mandatory submissions to state institutions. These ratios are created from the balance sheets and income statements, but for some of them, additional stock market information is needed: P/E, EPS, etc. In addition to this, the author in [70] analyzed 111 different financial ratios. However, only 53 ratios were used for predicting firm failure, which were selected using a two-sample t-test. In general, researchers use approximately 20–30 financial ratios for financial distress identification [3,26,66,71,72,73,74]. Of course, researchers are adding not only financial indicators, but other novel features that can be categorized as macro indicators, industry indicators, and additional indicators. The following Table 2 provides only direct indicators, not derived ones. For example, CEO age, not the log of CEO ages [75], or tenure, expertise, and education diversity, not its sum named as cognitive diversity [23], etc. In addition, these indicators can be used to create graphs, such as shareholder or manager connection graphs [76]. Moreover, this table can be supplemented with regulatory indicators, such as tax rate, economic freedom, the integrality of the legal system, regulatory, etc. [33]. Table 2 is like a guide map for future researchers, who want to know what kind of additional indicators (except financial) were used in previous studies.

The use of additional indicators spreads data and leads to a higher-dimensional space. Therefore, dimensionality reduction techniques are used to simplify model design and to create more efficient models. Our previous study’s findings, which examined 15 different methods for dimension reduction, led to the selection of the most effective methods, which were then utilized in this study. The chosen methods come from the embedded methods category, where both feature selection and algorithm training is conducted simultaneously. One of these techniques is called the least absolute shrinkage and selection operator (LASSO). This method removes uninformative predictors from the model by reducing their coefficients to zero [77]. An interesting aspect of the LASSO method, i.e., the stability of it over time, was analyzed in [24]. In the initial year, LASSO identified seven significant features, followed by nine features in the subsequent year, with only four of them overlapping consistently between both years. In [78], the same four features were selected from a set of 12 financial features using the LASSO method, backward and forward stepwise LR techniques. However, the study analyzed only 492 Vietnamese-listed enterprises and the results were compared with the Altman z-score. Another noteworthy study [79] incorporated the LASSO technique after the Q-Bert and BertTopic analyses of the text-based data. These data are question-and-answer (Q&A) information from online interactive platforms about investor concerns and companies’ reactions to them. The generated 187 topics were reduced to 71 topics after LASSO filtering.

Another popular embedded technique that is frequently used for detecting financial distress is XGBoost. Following the XGBoost importance rank, the top k features, that represent 80% of the feature importance overall were included in the study [80]. However, it is not explained how 80% is chosen for the determination in this research. Moreover, during the research in [81], four features were selected from 13 without further explanation. However, these features differ during pre-COVID and post-COVID periods. The feature set size limitation is also detected in the study [82], where only the random forest (RF) method is applied. Also, the authors used the correlation criteria (greater than 0.7) to select 25 significant features. The authors in [83] determined the optimal feature set by combining the random forest and the recursive feature elimination (RF-RFE) methods. Nonetheless, the feature set kept changing according to the predicted time window shift. In addition, the [84] study determined the optimal feature set by combining several different feature selection techniques (T-test, RFE-SVM, and RF) and selecting the features that overlap the most. However, it remains unclear where the optimal set is if the RF method ranks all provided features.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 2.

Indicators used for financial distress/bankruptcy detection.

| Category | Feature | ||

|---|---|---|---|

| Macroeconomics features | 10-year bond yield|Long-term interest rate [31,33,85]; 1-year treasury bill|Risk free rate [30,58,86]; Business lending rate [32]; Bank rate and wholesale price index (WPI) [31]; Brent barrel price [86]; Case–Shiller index [86]; Closure measure (i.e., the number of weeks the enterprise has been closed during the pandemic) [87]; Consumer price index [33,58,86]; Current account [33]; Equity indices rate [33]; | Eurozone (1 Eurozone country; 0 non-Eurozone country)|Region code [33]; Exchange rate [31,33]; Crisis episodes (dummy) [32,88]; GDP (Gross domestic product) growth rate (%) [31,32,33,39,58,85,86,87,89]; Government Debt [33,86]; Index of industrial production (IIP) [31,85]; Inflation ratio (%) [30,33,39]; Market premium [86]; Michigan confidence index [86]; | Money supply [31,33]; Nominal interest rate (%)|Real interest rate [31,33,58]; Repo rate|Short-term interest rate [31,33]; Retail price index [58]; Risk premium [33]; Unemployment rate [33,58,86,90]; Unit energy consumption [53]. |

| Industry features | Herfindahl–Hirschman index (HHI) [3]; Industrial risk [91]; Industry affiliation (dummy variable for industry (1–5)) [8]; Industry financial ratios (EBIT, EBITDA, working capital to assets, sales growth, etc.) [32,86] Industry growth [33]; | Industry–level|Industry ratios median [74]; Industry value rate [33]; NACE code (control indicator)|Industrial type|GICS Sector – industrials [25,33,53,63,77,87,90,92,93,94,95]. | |

| Additional features: (a) board, ownership, management | Board: Board networks [25]; Board qualifications [25]; Board size [3,15,25,38,53,68,72,77,96,97,98,99,100,101,102]; CEO serves as chairman simultaneously|Duality| Powerful CEO [3,19,25,53,58,88,96,97,99,100,102,103]; Cumulative voting [99]; Female director|Percentage of women|Board gender heterogeneity [15,68,77,87,88,96,97,98,102,103]; Foreign directors [88]; ‘Grey’ directors|Professionals [38,72]; Independent director| NEDs|Board independence [3,15,25,38,58,67,72,96,97,99,100,101,102]; Inside CEOs|Independent director monitoring [72,88,96,100]; Multiple directorships |CEO concurrent post [96,98]; Number of founders [77]; Outsider CEOs [38,72]; Staggered board [72,99]. | Ownership: Average share holding [96]; Blockholder ownership [99]; CEO ownership|Board shares [3,15,25,52,96,97,98,99,101,102,103,104]; Insider shareholding|Managerial ownership ratio [3,90,101,103]; Institutional ownership [15,58,96,97,103,105]; Major shareholders (more than 5% or 3 % of shares)[15,25,52]; Outsider ownership [99]; State ownership [3,58,87,96]; Supervisor shares [96,101]; The first major shareholders| Ultimate controller [3,53,58,72,98,102]; Top 3 shareholders [3]; Top 5 shareholders [3,90,106]; Top 10 shareholders [3,58,90,96,106]; Share capital change [58,96]; Large shareholder connection [96]; Listing elsewhere [96]; Type of ownership [93]. | Management: CEO|Founder age [88,96,98,103,107]; CEO option value|Total compensation|CEO paid [25,96,103]; CEO succession [67]; CEO|Chair postgraduate [96]; CEO|Chair|Founder professional qualification [96,107]; Change in management [58,77]; Independent audit committee [15,25,102,103]; Number of senior managers [96,101]; Number of supervisors [96]; Salary of seniors [96]; Salary of top 3 directors [58,96]; Salary of top 3 senior managers [96]; Salary of top 3 seniors [96]; Size of audit committee [15,25]; Tenure of CEO [25,77,88,98,100,102,103]; Top manager’s years of experience in the sector [77,87]; Turnover of CEO in previous 3 years [103]. |

| (b) Enterprises | Enterprises: Age of the enterprise; Audited [4,73,108]; Auditor’s opinion (Favorable|Qualification|Unfavorable)|Big4 auditor [4,73,109]; Audit fees [109]; Delay of annual reports [73,96]; Competitiveness [87,91]; Credibility [91]; Innovation [77,87,107]; Intellectual capital [92,110]; Location|Region [77,87,93]; Linked to a group (if the company is part of a group holding) [4,73]; Market (local, national, international) [77,87]; Number of business segments [90]; Number of changes of location [4,73]; Number of partners [4,73]; Relational capital| public contract and political connections [68,77,106]; Operation information changes [55]; Quality certificate (internationally recognized) [87]; Risk committee [109]; Size: (a) The log of the total assets; (b) Natural logarithm of turnover; (c) The market capitalization; (d) Micro|Small|Medium|Large [4,8,33,38,67,73,85,89,97,100]; Tax aggressiveness [111,112]; Type of company (public companies|Limited liability companies (Ltd))|Others) [4,73,87,93,94,108]. | Employees: Education level of employees [77]; Employment retention [113]; Employee tenure [77,77]; Equipment per employee (EPE) [104]; Equity per employee [94]; Female percentage [77]; Firing ratio [77]; Hiring ratio [77]; Number of employees [4,73,94,114,115]; Number of employees representatives on board [88]; Sales per employee (SPE) [104]; Unemployment rate of firm’s department [94]; Working capital per employee [94]. | Judicial incidents: Amount of money spent on judicial incidences (since the company was created) [4,73,108]; Amount of money spent on judicial incidences (Last year) [4,73,108]; Asset restructuring|replacement [58]; Dishonest debtor [58]; Equity transfer [58]; Executions enforced by the court [58]; Litigation [109]; Lawsuits (as defendant or plaintiff) [58]; Lawsuits type (corporate lending, breaching of contract, etc.) [58]; Number of judicial incidences(since the company was created) [4,73]; Number of judicial incidences (Last year) [4,73]; Previous patent applications [107]. |

| (c) Environmental: | Climate change disclosure performance [109]; Environmental pillar score [95]; Green tax [53]. | ||

| (d) Social responsibility: | Average of net corporate exchange capital [85]; Average of net corporate moral capital [85]; Average of net corporate social responsibility [85]; Corporate social performance (CSP) [67]; Corporate social responsibility (CSR) [19,85]; Social pillar score [95]. | ||

| (e) Social sentiment: | Sentimental categories: (a) Lexicon-based [55,116]; (b) Machine learning based (i.e., a bag of words, word embedding, etc.) [54,59,117,118]; (c) Hybrid [119,120]. | ||

In conclusion, financial distress is not a legal status of the enterprise. Therefore, out of the various financial distress indicators identified, 29 of them could be applicable to a public company, and 14 of them are suitable for SMEs. Moreover, a trend to add additional non-financial features to the analysis was noticed. These features were characterized into three main groups: macroeconomics, industry, and additional. Furthermore, the additional group is further divided into: (a) board, ownership, and management features; (b) enterprise additional features; (c) environmental; (d) social responsibility features; (e) social sentiment features. The most popular groups were board, ownership, management features, and enterprises’ additional features, among which the most common features used in the analyses were as follows: the age of the enterprise, size of the enterprise, board independence, board size, etc. However, the inclusion of additional indicators spreads the data and leads to a higher-dimensional space. Based on the findings from our previous study, we suggest using embedded methods for feature selection. On the other hand, a literature analysis has shown the remaining gap between the feature ranking and the optimal feature set.

2.2. Balancing Techniques

Class imbalance occurs when one class in a dataset has fewer instances than the other class [6]. Classification models often presume the equal representation of all classes. For this reason, a model may overlook financial distress enterprises (minority class) and classify firms as non-financial distress (majority class). Hence, a large skew to a single class causes classification algorithms to be biased toward the majority class [121].

In a real-world scenario, even during times of crisis, only a small number of all enterprises are in a state of bankruptcy [2]. However, the percentage of financial distress enterprises is greater than the ones that go bankrupt, and it typically falls between and , whereas the percentage of bankruptcy is between and [57,121]. Therefore, it is challenging to create a model for identifying financial problems.

Generally, the class imbalance approaches are divided into data level, algorithm level, and hybrid approaches. The data-level approach (also called sampling-level) creates a more balanced distribution of classes using preprocessing techniques, such as oversampling, undersampling, or a hybrid approach [2]. The algorithm-level approach modifies the classifier to prioritize learning how to distinguish the minority class using such techniques as cost-sensitive learning and ensemble learning [120]. Combining these two approaches creates a hybrid methodology, which modifies the classifier and the data to solve particular problems [9]. The comparison of these techniques is presented in Table 3.

The problem of class imbalance in financial distress research is solved in three ways:

Typically, the first group of researchers uses a data-level approach, and mostly uses the Synthetic Minority Oversampling Technique (SMOTE) [24,34,54,93,137,138,139], or the random sampling (undersampling) [77,145] or random sampling with the matching parameter (sector, size, etc.) [50,140,141,142,143], also called stratified sampling [144]. Due to its relevance to this article, the second research group will be analyzed more in-depth.

The utilization of data-level approach combinations is more frequently observed in comparison to algorithm-level combinations, owing to the independent creation of processes from sampling and classifier training, and the ability to utilize a wider range of machine learning algorithms in subsequent analyses. Researchers usually involve random oversampling (ROS), random undersampling (RUS), and SMOTE techniques in the analysis [6,124,132] or analyze the improvements of SMOTE methods among themselves [4,108,121,134]. Veganzones and Séverin (2018) [124] analyzed ROS, RUS, SMOTE, and easy ensemble techniques with different class imbalance ratios and machine learning approaches. The following machine learning algorithms were included in the research: linear discriminant analysis (LDA), logistic regression (LR), neural network (NN), support vector machine (SVM), and random forest (RF). The authors demonstrated the significance of utilizing balancing techniques, resulting in a decrease in machine learning performance power when the ratio of class imbalance is ≤. However, the SVM method turned out to be less sensitive to an increase in class imbalance. Moreover, SMOTE offered the best results. Other bankruptcy prediction researchers for Slovak SMEs [6,132] analyzed ROS, RUS, and SMOTE techniques with AdaBoost, the C5.0 algorithm, CART, CatBoost, LDA, LR, and NB classifiers. The best AUC performance (99.95%) was obtained with stepwise regression for feature selection, the ROS sampling technique and the CatBoost algorithm. Without using feature selection techniques, the highest AUC (99.94%) was reached with the SMOTE sampling technique and the CatBoost algorithm. Without using feature selection techniques, the highest AUC (99.94%) was reached with the SMOTE sampling technique and the CatBoost algorithm. Moreover, in study [146], the ROS sampling technique overperformed other data-level approach techniques (RUS, SMOTE, and a combination of SMOTE and the Tomek links (SMOTE-TL) with gradient boosting tree algorithm (Gboost) for a dataset of Polish enterprises, reaching an AUC score of 78.7%.

The authors in [108] used a Spanish bankruptcy dataset to analyze data-level approach techniques: SMOTE, borderline-SMOTE (BSMOTE), Safe-level-SMOTE, ROS, RUS, condensed nearest neighbor together with different individual algorithms (SVM, C4.5, and logistic regression), and ensemble learners (AdaBoostM1, DTBagging, and RF). The best AUC score (99.98%) was achieved with DTBagging and two of the sampling techniques: BSMOTE and ROS. The BSMOTE algorithm was analyzed in [134] along with SMOTE, Adasyn, a combination of SMOTE and the Tomek links (SMOTE-TL), and a combination of SMOTE and the edited nearest neighbor (SMOTE-ENN). However, the authors used principal component analysis (PCA) on a Korean dataset before applying the sampling techniques, which resulted in additional difficulties in properly distinguishing the classes. For example, if SMOTE is performed before PCA, maintained class trends are observed, whereas after performing PCA, the points selected by the SMOTE method are more scattered. Nevertheless, authors used RF, DT, NN, and SVM classifiers for predicting the bankruptcy. The best AUC results (84.2%) were achieved with SMOTE-ENN and RF. The authors in [121] compared the SMOTE method and its different modifications: Adasyn, Adasyn, BSmote, DB Smote, Safe-Level Smote, and a combination of SMOTE and cluster-based undersampling. This study analyzed quarterly data from a US company, obtained from Bloomberg, using 11 different machine learning algorithms, including LDA, LR, SVM, etc. The highest AUC score (95.6%) was reached with NB and ADASYN.

In the [2] research, which analyzed the algorithm-level approach, these one-class classifiers were used: one-class SVM, isolation forest (IF), and least-squares anomaly detection (LSAD). The bankruptcy prediction results for Slovak SMEs demonstrated that LSAD had outperformed the other predictors, having the highest AUC prediction score (91.83% for the construction sector and 87.92% for the manufacturing sector). Another research [82] analyzed the EasyEnsemble and the BalanceBaggingClassifier for US company data. This research achieved an AUC score of 93.9% by implementing XGBoost with the EasyEnsemble technique for financial and textual data.

Moreover, researchers conduct comparative analyses not only among techniques employed in a single approach, but also among diverse approaches (as illustrated in Table 3), in order to predict financial distress or bankruptcy. For example, the [4] analysis proved that SMOTE combined with the AdaBoost ensemble method using a basic classifier (the REP tree) can produce promising (and dependable) results (AUC = 87%). Furthermore, the bankruptcy of Slovak SMEs was predicted in an extensive study ([5]) about the usage of algorithm-level techniques. The analysis was conducted using AdaBoost, RF, gradient boost (GB), balanced bagging (BB), easy ensemble, balanced random forest (BRF), RUSBoost, one-class SVM, and IF. Moreover, this study analyzed the annual distance from bankruptcy, from one year to four. The findings of this study distinguish themselves from other studies due to the superior outcomes achieved two years prior to bankruptcy compared to one year, and the highest G-mean score of 97.4% was achieved using the RUSBoost technique. Another study [51,57] proposed using a technique called weighted XGBoost-based tree (XGBoost-W-BT). To compare the results, different data-level techniques were used like ROS, RUS, and SMOTE. Also, algorithm-level techniques like AdaCost, MetaCost, and cost-sensitive boosted trees, as well as hybrid III techniques like RUSBoost and SMOTEBoost were used to compare the results. Even though different authors presented the results of these studies in separate articles [51,57], it is worth noting that both papers share the same analysis and results. However, the specific ML methods employed for the data-level approach are not fully disclosed, i.e., it is unclear what additional techniques were used along with SMOTE. Nevertheless, the proposed model demonstrated the highest scores.

Often, the authors want to confirm the effectiveness of a newly proposed sampling technique by demonstrating its suitability through experiments. For example, E-SMOTE-ADASVM-TW model embeds SMOTE into the iteration of the ADASVM-TW model [1], multi-objective classifier selection (MOCS) [126], or the adaptive neighbor SMOTE-recursive ensemble approach (ANS-REA) [3]. Nevertheless, the proposed techniques were not empirically tested in other studies.

Moreover, the effectiveness of deep neural networks suggests its use regarding the topic of class imbalance. The generative adversarial networks are used to generate synthetic samples in different fields: image generation [147], intrusion attack samples [148], tabular data [149], etc. For example, the authors in [150] firstly used GAN to generate bankruptcy samples. This GAN was used together with heterogeneous graph neural network algorithm, and outperformed undersampling, oversampling, SMOTE, and re-weight techniques, achieving an AUC score of 71.4% for the Tianyancha dataset. However, this method was not compared to other class imbalance techniques.

In conclusion, data-level approach application prevails in financial distress and bankruptcy topics. Primarily, the SMOTE technique and its various modifications are employed.

3. Data

3.1. Sample Size

LTD Baltfakta collected and provided the dataset used in this study. It contains information on 64,648 active enterprises operating in Lithuania, covering the period from 1 January 2015 to 30 December 2022. The analyzed enterprises meet the following conditions:

- Small- and medium-sized enterprises (SMEs). The enterprise category is defined according to the last consolidated version of the European Union Commission Regulation (EC) No 651/2014 [151]. Medium-sized enterprises are made up of enterprises that employ fewer than 250 persons, which have an annual turnover not exceeding EUR 50 million and/or an annual balance sheet total not exceeding EUR 43 million. A small enterprise is defined as an enterprise which employs fewer than 50 persons and whose annual turnover and/or annual balance sheet total does not exceed EUR 10 million. A micro-enterprise is defined as an enterprise which employs fewer than 10 persons and whose annual turnover and/or annual balance sheet total does not exceed EUR 2 million. The number of employees is defined according to the Order of the Minister of Finance of the Republic of Lithuania No 1K-320 [152]:where —mean number of employees in the analyzed year; the indicator from 1 to 12 corresponds to the last day of the months (i.e., 1—January, …, 12—December) from which the number of employees is taken. —indicates the number of employees on December 31 of the previous year; or —indicates the number of employees on December 31 of the analyzed year. The size change of analyzed enterprises during the years is represented in Figure 1. During the analyzed years, the enterprise change in the non-analyzed category (highlighted in gray) occurs due to the removal of enterprises that have experienced financial distress (for the recovery period) or the inclusion of new enterprises in the sample (related to the establishment of new enterprises or the end of the recovery period).

- The legal form of an enterprise is assigned to one of these categories: (a) a private limited liability (PLL); (b) a public limited liability (PbLL); (c) agricultural enterprise (Agr); (d) an individual enterprise (Ind); and (e) a small community (SCom);

- Enterprises excluded from this analysis belong to these NACE sectors: K—financial and insurance; L—real estate; O—public administration and defense, compulsory social security. The distribution between the NACE code and the legal status of the analyzed enterprises is provided in Appendix A;

- The enterprise’s age is ≥1.5 years;

- The enterprise has provided at least one financial statement from the last two years;

- The enterprise has ≥1 socially insured employee (only for legal form: PLL or PbLL);

- The recovery period ≥ 1 has passed. The recovery period depends on the external reaction of market participants. If the financial distress status is obtained from the information supplied by the authoritative institutions, then the enterprise has to register the resume of its activities and maintain good enterprise conditions for at least 1.5 years to be considered again as a non-financial distress enterprise. For example, an enterprise has had a bankruptcy case in court before, but following a change in circumstances, the enterprise’s operations persist, and its favorable conditions are acknowledged in the LTU register. If the financial distress status is obtained through Financial statement information, the recovery period is 1 year after the fulfillment of non-financial distress enterprise requirements.

The final dataset consists of 184,421 unique records, of which only ∼10% of the cases represent financial distress. The data are split into training and test datasets. The test dataset covers the latest period, i.e., the class variable is based on the year 2022, and the training dataset consists of class identifiers covering the period from 2018 to 2021. Thus, the dataset is divided into training and test datasets according to a ratio of ∼75:25.

3.2. Class

In this study, a binary classification problem was analyzed, where 0 indicates “non-financial distress”, also known as a “good” enterprise, and 1 indicates “financial distress” in the enterprise. The state of combined financial distress is defined by several financial distress conditions:

- Institutions’ financial distress (Institutions FD);

- Employees’ financial distress (Empl FD);

- Debt financial distress (debt FD);

- Financial statements:

- (a)

- Equity financial distress (Equity FD);

- (b)

- Net income financial distress (Net income FD).

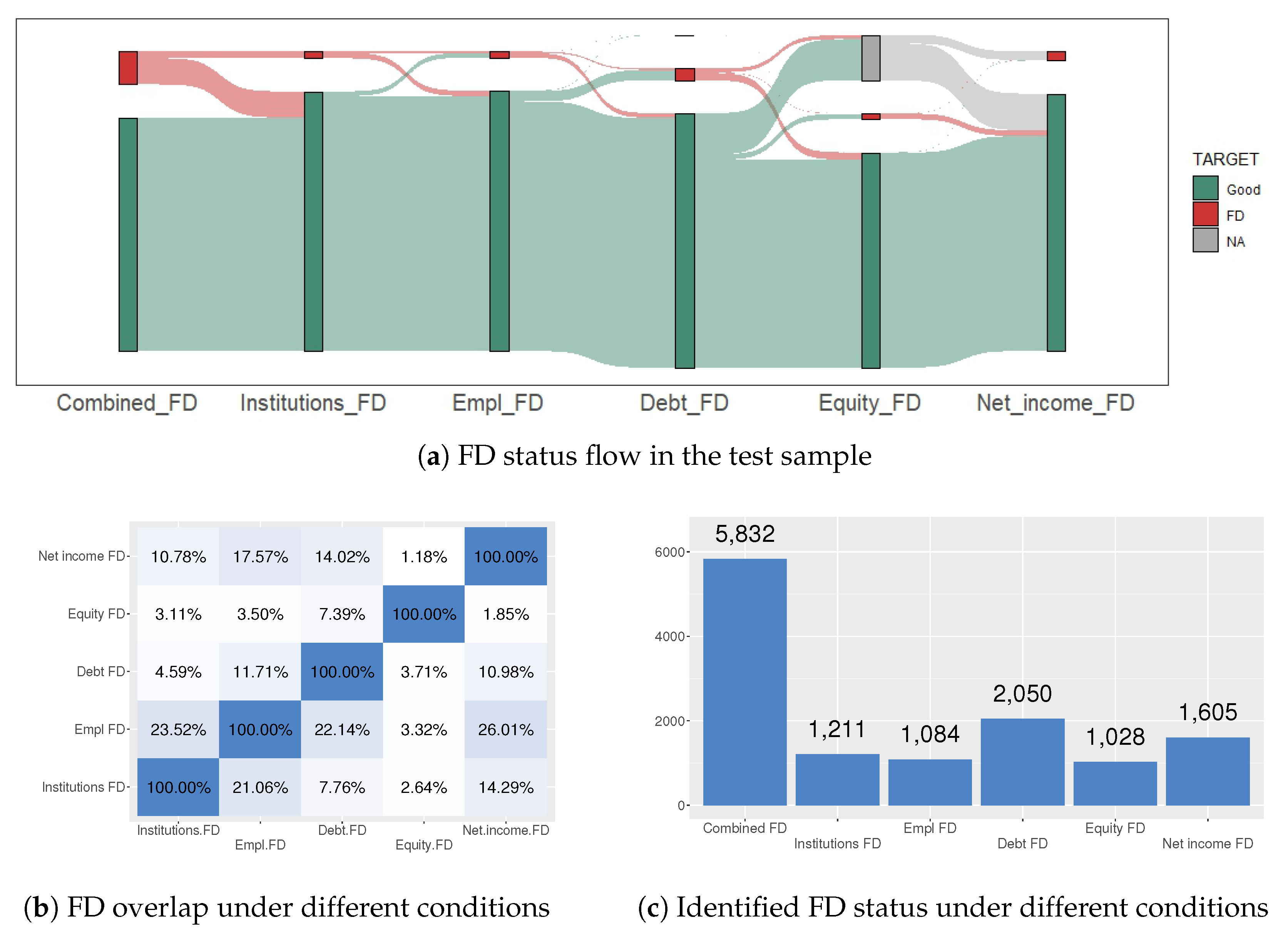

All of these definitions of financial distress conditions are presented in Section 4.1. They are connected by the “OR” operator for final financial distress determination. The distribution of the financial distress condition in the training and test sample is presented in Figure 2 and Figure 3. Comparing Figure 2a and Figure 3a, it is noticeable that the NA values of Equity_FD are higher in the test dataset. The reasoning behind this is as follows:

- The enterprise has not submitted a financial statement on time. The financial statement was downloaded on 12 July 2023. According to the law, enterprises must submit the FS 6 months after the end of the period;

- The enterprise submitted a misleading financial statement (see Section 4.1.4);

- The enterprise’s FS period is different.

From Figure 2b and Figure 3b, it is observed that there are not many overlaps between different financial distress conditions. A more intense color in Figure 2b and Figure 3b indicates greater overlap. The y axis of these graphs represents the overlap of one FD status over another FD status, i.e., Figure 2b Institutions FD overlap EMPL FD by 54.89%, but EMPL FD overlaps institutions FD by only 22.05%. FD statuses are affected by the difference in the number of cases (see Figure 2c Institutions FD—1146, Empl FD—2853). Also, it can be noticed that Debt_FD determines the highest number of FD conditions for enterprises (see Figure 2c and Figure 3c).

3.3. Features

The data used in this research can be divided into nine different categories, depending on the provider of the data or the information (see Table 4). For example, three data source providers are combined in the sector’s category: (1) sector type, identified by the NACE category; (2) information on sector profitability, competitiveness, etc. from the Lithuanian Statistics Department; (3) sectoral indicators calculated by combining financial statement data and NACE types. The number of features shows how many features fall under this category. The data frequency is divided into three categories:

- Stable—information is constant, e.g., legal status, types of sectors;

- Depending on an event—changes when the event occurs, the number of courts, the number of changes of directors, the time elapsed since the last event, etc.;

- Periodic data (annual, quarterly, monthly)—information is updated at the indicated periodicity, e.g., financial reports, macro indicators, and the number of employees.

Periodic data correspond to time series data. Each period interval was treated as a separate feature. For example, from the balance sheet the feature “Total assets” (see Appendix C) is presented annually, therefore, the features of “total assets” are analyzed separately for the periods , and . The same condition was applied to the monthly data: the number of employees had been collected 36 times (i.e., monthly data for three years) along with various change statistics. The methodology’s concept is based on demonstrating AI’s ability to select important attributes without human intervention. Surprisingly, the conducted experiment revealed that the company’s debt in period is more significant than in period .

All categorical features have been transformed into binary features by expanding the feature space. In the final dataset, each enterprise is described by 1016 features for each analyzed year.

4. Methodology

The aim of this research is to analyze the balancing technique’s influence on identifying financial distress. For this reason, various class balancing techniques were implemented in combination with different feature selection and machine learning methods. Hence, the focus of this research is to answer these questions:

- RQ1:

- What is the difference between machine learning model performances for different financial distress conditions?

- RQ2:

- How does the use of different feature selection techniques affect the results? Do selected features have the same patterns?

- RQ3:

- Which strategy is more effective for determining the size of features: an experimental or rule-based approach?

- RQ4:

- Which method of class balancing is the most effective for identifying financial distress?

- RQ5:

- Which machine learning model performs better in identifying financial distress?

The proposed framework for identifying financial distress is presented in Figure 4.

The first step deals with identifying primary conditions: expansion of class definition (see Section 4.1) and preparation of the final feature space (see Section 4.2). After creating the final dataset, the data are split into training and test samples. Cross-validation is not performed in order to obtain the classification evaluation results on the most relevant data and to provide market participants with current information about enterprises’ financial distress position. Hence, the test dataset uses the newest data and the training dataset uses data from 2018 to 2021. The ratio of the total data to the training and test samples is about 75:25.

The second step is data normalization. Normalization is a critical step in developing classification models with equal feature scales, i.e., it is performed to limit the dominance of specific features. The normalization process begins with the normalization of the training dataset, and then these normalization characteristics (identified by 2* arrow in Figure 4) are saved and used for normalizing the test dataset.

For the latest period data (test data), normalization is based on the features’ characteristics from previous years. Min–max normalization is used to scale the variables between zero and one [153]:

where is an original value of the j feature; —the transformed value of the feature j; and are, respectively, the minimum and maximum values of a feature.

After normalization, all missing values (NA) are replaced by the smallest value—zero.

The third and fourth steps are related to the selection of important features and the identification of an optimal feature set. Firstly, feature selection techniques (see Section 4.3) rank the feature set in decreasing order of importance. The feature set is then narrowed down based on the chosen strategy: the experimental max number or the rule-based strategy (see Section 4.4).

The fifth step is either balancing or sampling the data. In this research, several oversampling, undersampling, and hybrid sampling techniques were used to give a better representation of the minority class instances (see Section 4.5). In addition, the non-balanced training dataset is also included in the comparison.

The sixth step is model training. Supervised machine learning classification methods, which are specified in Section 4.6, were used for identifying financial distress.

The seventh and eighth steps show the results after the classification and evaluation of the test data. The evaluation metrics are described in Section 4.7.

4.1. Class Definition Conditions

4.1.1. Financial Distress Identification from the Authoritative Institutions Perspective

The class being determined by the authorities is the worst-case of a financial distress scenario, as the chances for the enterprise to stop the bankruptcy or liquidation processes and recover are very little. Three authoritative institutions were analyzed as the main providers of information for identifying Institution’s financial distress:

- Registry center;

- State tax inspection;

- Courts.

Institutional financial distress class definition includes the following:

- A bankruptcy case that is filed against the enterprise;

- The enterprise’s status in the register center being changed to going bankrupt, bankrupt, under restructuring, under liquidation, etc.;

- The enterprise having made announcements to the register center about bankruptcy, liquidation, restructuring, insolvency, etc.;

- The enterprise being included in the State tax inspectorate’s lists of:

- (a)

- Companies temporarily exempt from submitting declarations to the STI,

- (b)

- Companies that have declared temporary inactivity to the STI;

- (c)

- Companies for which the STI has submitted a proposal to the State Register for deregistration following Article 2.70 of the Civil Code.

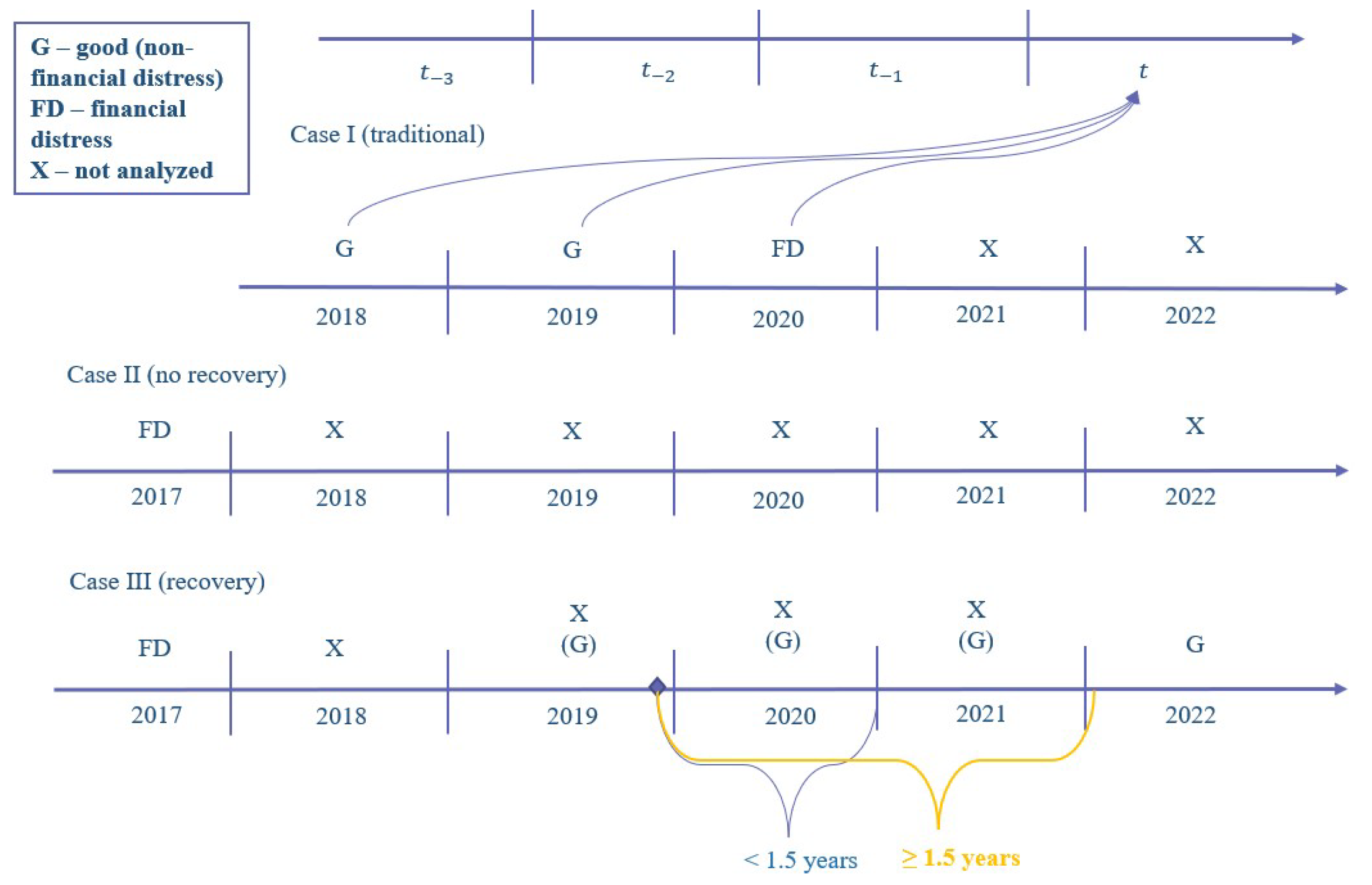

The enterprise may experience several of these events at once. For instance, an enterprise might be listed in the STI (State Tax Inspectorate) while its status in the registry center is marked as ‘under liquidation’. In such case, the earliest date of the first incident is determined. The enterprise is then placed in the FD category and is not further examined until the recovery criterion is satisfied. Notwithstanding, the likelihood of an enterprise satisfying the recovery criterion, i.e., the enterprise’s status changing to no legal proceedings in the registry center, is low. This is classified as the beginning of a recovery event, and after the 1.5 year recovery period is over, the enterprise is then included back into the sample (see Figure 5).

4.1.2. Financial Distress Identification from the Drop in Employees’ Perspective

A sudden decrease in the number of employees in an enterprise’s activities indicates an unclear internal situation of the enterprise, which can be linked to financial distress. However, the identification has to be made after the seasonality condition is checked.

For finding stable seasonal patterns, the Kruskal–Wallis test is used [154]. The selected significance level is , i.e., smaller p-values suggest that there are indications of seasonality in the time series. Seasonality is analyzed for enterprises that meet these conditions:

- The minimum number of employees has to be >0 during the t and years;

- The mean of employees ( see Equation (1)) has to be >5 and <250 during the year;

- Available information about employees in an enterprise is ≥26 months.

Every year, the seasonality of enterprises is checked. If the enterprise meets the requirements to qualify as a seasonal one, it is included in the list of seasonal enterprises.

It is evident that due to the time series being too short, determining the seasonality of some enterprises will not be possible. For this reason, sectors with the greatest seasonality (according to NACE: A, B, C, F, G, I, see Appendix A) had been identified and were considered, just like the Agr enterprises, as seasonal enterprises.

Employee’s financial distress class definition includes:

- If the minimum number of employees is >0 in period t:

- The maximum number is >5 in period t, and the enterprise is not indicated as seasonal, i.e., is not included in the seasonal enterprise’s sample or is not assigned to seasonal legal status or enterprise sectors. If all conditions are satisfied, then the following indicators are calculated:where —the number of employees on December 31 of the period t; M—median of the number of employees during the year, max—max number of employees during the period t, —the number of employees on January 31 of the period t.After calculating the indicators, the change is analyzed, and if the change meets at least one of the conditions specified in Table 5, the enterprise is identified as being in financial distress.

- If the minimum number of employees = 0 in period t:

- (a)

- For ≥3 months:

- Legal status is PLL or PbLL;

- (b)

- For <3 months:

- The maximum number of employees is >5, the minimum number of employees is >0 in period , and the enterprise is not indicated as seasonal. The conditions of seasonality and financial distress are the same as in the first case.

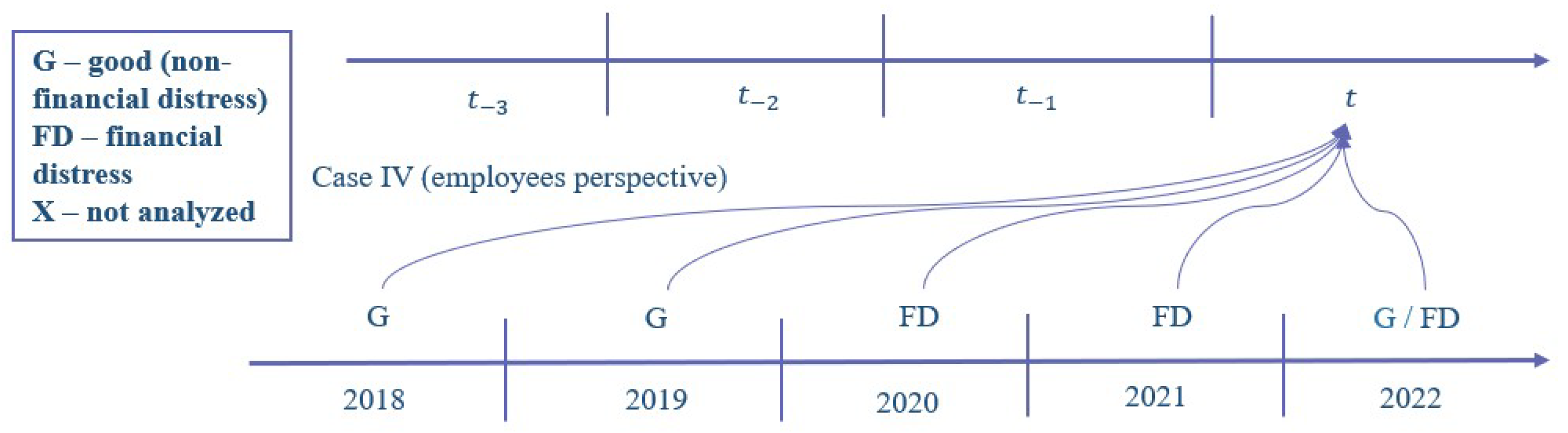

These conditions do not encompass all micro-enterprises due to the insufficient number of employees required for seasonality determination and implementation of drop in employees perspective. Moreover, the recovery criterion is not implemented, which allows the enterprises to have FD status for two consecutive years (see Figure 6).

4.1.3. Financial Distress Identification from a Debt Perspective

The enterprises having overdue financial obligations is a key indicator of financial distress. However, the availability of this kind of data is limited. The Lithuanian government gave information to the State Social Insurance about how many people work for the enterprises without paying social insurance taxes. The debt information was not used for identifying financial distress. Since the size of the debt depends on the size of the enterprise, a debt of 10,000 EUR is large for one enterprise, but small for another. For this reason, we created a flexible indicator—, see Equation (6):

where the indicator shows how deep in debt an enterprise is if it pays minimal month’s salary (MMS) to its employees; —max debt during the period t, and calculation is shown in Equation (7):

where —indicates a minimal amount of payment, i.e., cases where employees did not work for a full month and have been paid more than the minimum wage are not analyzed. —mean number of employees in period t; —the minimal month’s salary in period t (see Table 6). The indicator 0.2 is a minimum state social insurance tax payment from brutto salary for the employee.

Debt financial distress class definition is:

- If ≠ 0:

- ≥ 3 and Debt is overdue for ≥90 days.

- If = 0:

- (a)

- Legal status is PLL or PbLL:

- Debt is overdue for >15 days.

- (b)

- Legal status is Agr, Ind, or SCom:

- ≥ 3 and debt is overdue for ≥90 days.

The second condition is noteworthy due to the legal nature of the Agr, Ind, or SCom enterprises, i.e., enterprises, which provide opportunities for employment without the need for socially insured workers. Therefore, a correction in the formula is made by removing the zero indicator ():

However, Agr, Ind, or SCom enterprises can operate without employees, and the possibility of debt to this institution becomes questionable. Nevertheless, the debt overdue is smaller, for PLL or PbLL enterprises due to the unclear situation with these enterprises.

The recovery criterion is not implemented, as in the drop in employee’s perspective (see Figure 6) which allows the enterprise to have an FD status for two consecutive years.

4.1.4. Financial Distress Identification from Financial Statements Perspective

The identification of financial distress from financial statements is widely analyzed in the literature (see Table 1). As a result, two indicators were chosen for recognizing financial distress:

- Equity (negative) for period t;

- Net income (loss) for t and consecutive periods.

To clarify, the main reasons behind choosing these indicators are as follows:

- NA (not available data) values being present in financial statements. The deeper a subcategory in the statement is, the fewer areas are filled, e.g., interest expense is filled only 12–33% depending on the analyzed year. The completion level of a financial statement is given in Appendix B. Also, NA values double, if a ratio is present;

- unsuitability for SME analysis, e.g., if total liabilities divided by Total Equity is chosen as an indicator, almost all FD enterprises would be present, due to the main financing coming from equity.

- Overlaying results, i.e., net loss overlays 100% of the negative earnings results and ∼96% of the operating profit results.

Misstatements are eliminated before the financial statements are analyzed. For a financial statement to be considered for this analysis, it has to have:

- Balance sheet:

- (a)

- Total assets = long-term assets + short-term assets

- (b)

- Total equity and liabilities = equity (net worth) + amounts payable and liabilities + grants and subsidies

- (c)

- Amounts payable and liabilities = long-term amounts payable and liabilities + short-term amounts payable and liabilities

- (d)

- Total assets ≥ 0;

- (e)

- All statements in balance sheet ≠ 0.

- Income statement:

- (a)

- All statements in the income statement ≠ 0;

- (b)

- All profits (gross, operating, net) ≠ 0;

- (c)

- All costs ≠ NA or opposite sign. Here, ‘opposite sign’ implies that costs which increase profit do not decrease it.

In the analysis, only enterprises, which have provided at least one financial statement from the last two years, are included. For this reason, NA values are treated as FD conditions of previous years, see Table 7.

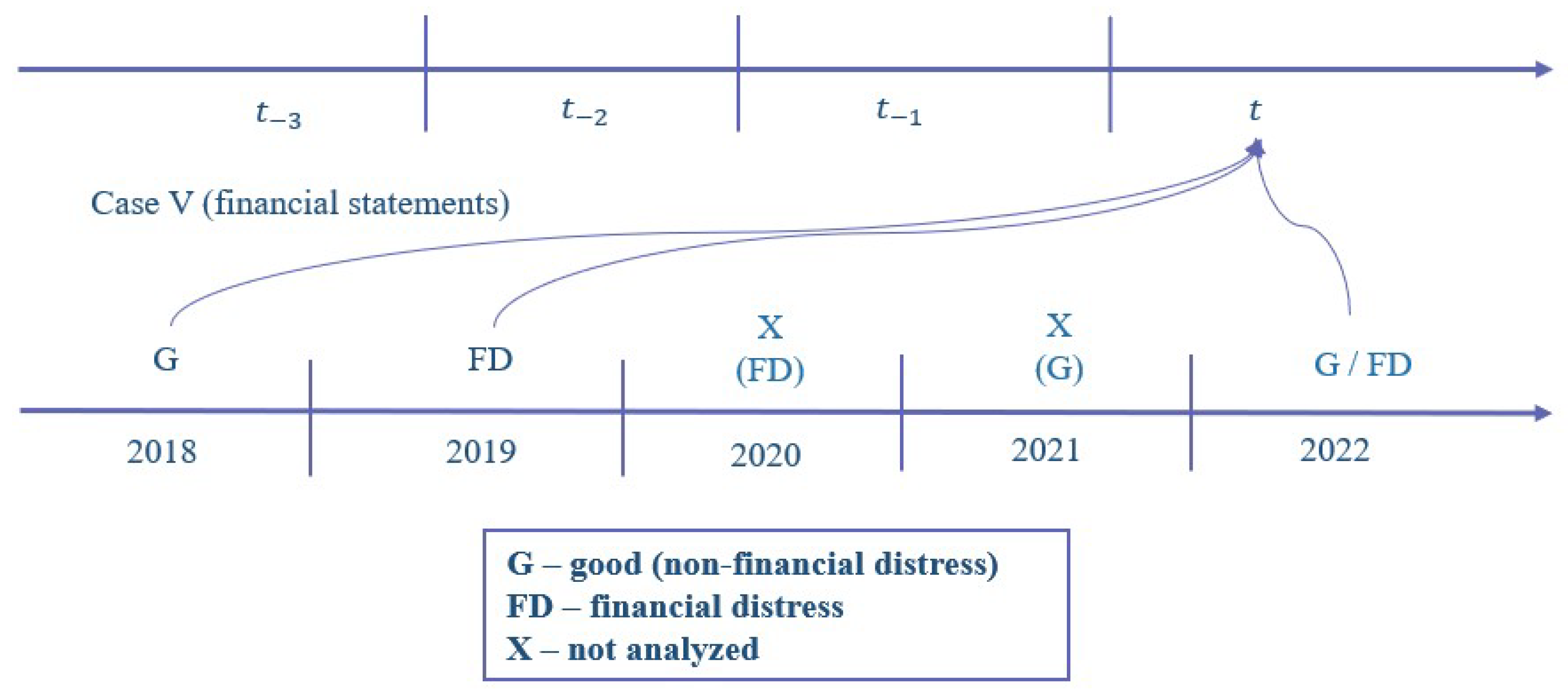

The financial statements of enterprises are not analyzed until their recovery period has passed. The criterion of recovery for financial statements is shown in Figure 7.

4.2. Feature Set Preparation

The list of all features is presented in different tables sorted by data category (see Table 4) and shown in Appendix C. However, not all features are included in the analysis due to not having variance. These features are crossed out in Appendix A and eliminated from the study.

The selection of financial ratios for inclusion in the analyses has been based on the fulfillment of financial statements (see Appendix B), with a minimum of >50% of filled values (not NA) being considered. These values are not filled due to differences in FS templates for enterprises, which depend on the size, legal form, etc., of the enterprise. Moreover, the percentiles’ method has been used for all financial ratios, i.e., all observations that lie outside the interval formed by the 2.5 and 97.5 percentiles are considered as potential outliers [156] and their values are changed to NA (not available data). However, this implementation has not been sufficient for some features, which is why the percentiles’ method was repeated. In Appendix D, the statistics of financial ratios before and after using the percentiles’ method are presented.

For all these time-related features, like the time after the director change or the last lawsuit, the Equation (9) is applied, after calculating the feature duration in days:

where is the number of days that have passed after the event, and is a derivative attribute, which indicates a greater significance the closer it is to the present. If is equal to 0, then is equal to 1.

4.3. Feature Selection Methods

The incorporation of new features into the model is related to detecting early warning signals and creating more precise models. However, the expansion of the feature space has a negative impact that occurs through data sparsity, multiple testing, multicollinearity, and overfitting problems [9]. To overcome these difficulties, different dimensionality reduction techniques are used. In this study (based on previous research), several embedded techniques have been used that belong to the feature selection approach. This approach determines a narrow subset of informative features from the original wide range of data [157] by removing irrelevant, redundant, or noisy features. Also, the embedded technique uses machine learning models for feature selection.

- LASSO (least absolute shrinkage and selection operator) is a method that combines feature selection and regularization. This method thins out the feature space by reducing some regression coefficients to zero [158]. The features that are left (non-zero) are then prioritized by the absolute value of LASSO regression coefficients. LASSO defines a limited group of features, which makes the interpretation of a model more accurate and is used for further classification [24].

- The random forest (RF) employs two methods for prioritizing features, both of which involve aspects of feature cost and the ability to differentiate [159].

- (a)

- (b)

- (Voted importance) prioritizes features depending on the combined rank from all the feature selection methods.

4.4. Number of Features

Despite the lack of information on the requirement for a maximum feature set for efficient model creation, the researchers focus on implementing the dimensionality reduction techniques. Hence, this research creates several new research directions to fill this gap.

- Experimental max number strategy narrows the prioritized feature set to an experimentally chosen number of features from a lower-dimensional space, specifically, .

- Rule-based strategy takes the most effective feature’s value, which is given by the embedded model, then splits it in half (), and all the features valued > go to a final dataset. Also, this strategy could be called half of the highest value strategy. According to this strategy, in this research, the k value for LASSO is 5, RF-MDA—36, RF-MDG—20, XGBoost—4. Since this strategy for the has to include 321 features, it was modified by only including overlapping features with ≥0.9 combined ranking score, then .

4.5. Class Balancing Techniques

Let denote the class labels, where n is the number of enterprises and belongs to one of the two classes: —non-financial distress (majority class) or —financial distress (minority class). Each enterprise is defined by a number of features , . The balancing ratio () of the training dataset T is:

The ratio’s values range from 0 to 1, the smaller the number, then the more difficult the task will be for a learner [135]. Financial distress and bankruptcy are rare events for the enterprises, and hence, the for these events is from 0.01 to 0.001 [124]. This lack of data from the minority class makes the majority classes dominate evaluation metrics, i.e., the learner can attain 99 percent accuracy without classifying rare examples [164]. For this reason, it is better to use AUC, Gini, G-mean, Recall, and Precision metrics [9].

The problem of class imbalance can be solved by using three different approaches: data-level, algorithm-level, and hybrid. The data-level approach involves modifying the data to ensure a more equitable distribution of classes. In contrast, the algorithm-level approach makes adjustments to the learner’s bias, prioritizing minority classes in the learning process. The hybrid approach combines data-level and algorithm-level approaches. In this research, the data-level approach, which separates the sampling and the classifier training processes, is used. To be more precise, the following techniques were employed:

- Oversampling—a technique, used to increase the amount of data. It modifies the original dataset by replacing or creating new data samples (generally the minority ones) [165]. The advantages of this technique include the enhancement of learner performance and a more precise representation of the two classes.

- (a)

- SMOTE (synthetic minority oversampling technique) is an oversampling technique that generates synthetic examples from the minority class to achieve a balanced dataset distribution [131,166]. SMOTE employs the k-NN method for the identification of the k-nearest neighbors of the minority class, and then generates synthetic examples by interpolating the reference sample with a randomly selected object from its neighborhood [167]. The SMOTE-generated samples are linear combinations between two similar samples from the minority class ( and ) and are defined as [166,168]:with generated synthetic samples; ; is selected at random from the 5 nearest neighbors (minority class) of .

- (b)

- SMOTE-NC (smote-nominal, continuous) is an enhancement of the SMOTE method, that generates data in a continuous or nominal way, by employing the modified-Euclidean distances as in Equation (12), depending on the feature type [169]in which is the distance between these observations; and are the number of continuous and nominal features, respectively; is the median value derived from the standard deviations of nominal features within the minority class [170,171,172]. If the features are continuous, is calculated according to Equation (11). Otherwise, for nominal features, the median value is determined based on the majority voting of the k-nearest neighbors vector, with the category, that appears most frequently, chosen as the value for the new observation [170].

- (c)

- ADASYN (adaptive synthetic sampling approach) was proposed by He et al. [173] and was based on the SMOTE algorithm [174]. However, the disparities arise in the selection of density distribution for the automatic generation of sample sizes for minority classes [173]. The ADASYN algorithm generates minority-class samples in areas that are more difficult to learn [174]. It also determines how many synthetic samples are required for every minority example to be created, based on how many of its majority class nearest neighbors are involved. The proportion of the majority nearest neighbors has a direct impact on the quantity of synthetic samples generated for the minority class.However, the “noise” sample detection is not included in this algorithm. Thus, near-borderline sample generation could lead to the creation of an unrealistic minority space for the learner [174].

- (d)

- GAN (generative adversarial networks) is an adversarial modeling framework of two multi-layer perceptron models: a generator (G) and a discriminator (D) [175]. The G task is the generation of a synthetic data sample, which would be identical to real data [149]. However, the G task is judged by a discriminator (D), which is a binary classifier for the recognition of the real data from generated [148]. GAN has shown success in complex high-dimensional distributions of real-world data, such as image generation, image-to-image synthesis, image super-resolution, etc. [147,148,149]. Nevertheless, the potential of GAN can be found when solving class imbalance problems, as it can generate samples of the minority class [147]. It is known that, in the best-case scenario, the training process continues until D can no longer recognize real samples from generated samples, i.e., the global optimal solution is obtained [148]. However, it can be stopped after reaching a specified number of iterations or at the local minimum [147]. The GAN optimization problem is defined as follows:where , , and are real training minority class samples, generated samples, and noise variable distribution, respectively; is a function of mapping noise to a data space, and shows the probability that the sample x is real data rather than a generated sample. The GAN is trained to maximize and to minimize [148,175].

- (e)

- ROSE (random over-sampling examples) is based on using a smoothed bootstrap approach for generating new synthetic data for the classes (minority and majority) [176,177]. This oversampling technique begins with estimating the multivariate probability density function (PDF) for each class. Then, this estimation is used to draw samples [178]. Essentially, an observation belonging to one of the two classes is extracted from the training dataset and a new sample is created in its neighborhood. The neighborhood’s shape is defined by the contour sets of K, with its width controlled by [165].

- Undersampling—a data cleaning technique, which reduces the original dataset by removing samples (usually belonging to the majority class) from it [165]. Decision surface cleaning, class overlap reduction, and ‘noisy’ sample removal are some of the main advantages of this technique [179].

- (a)

- The K-mean algorithm determines the cluster centroid by measuring the separation between each data point in the cluster, which is then used to cluster data [180]. Then, the algorithm detects and removes samples, that are in narrow, borderline, and noisy areas from the majority class until the intended balance is reached [181].

- (b)

- Nearmiss (removes points near other classes) is an undersampling technique, that eliminates the samples from the majority class by implementing the k-NN algorithm. The selected majority class samples for removal are near to some samples of minority classes [165,182]. Nonetheless, this method removes the points from the majority class, which have the smallest mean distance to the k-nearest points from the minority class.

- (c)

- RUS (random undersampling) is a non-heuristic technique that seeks to produce a balanced instance set by randomly removing instances of the majority class in order to balance the distribution of classes [165].

- The hybrid sampling technique combines both oversampling and undersampling techniques.

- (a)

- SMOTE-ENN combines the SMOTE and edited nearest neighbor (ENN) techniques and is assigned to the hybrid sampling technique group [183]. SMOTE is an oversampling technique, which generates synthetic samples for the minority class. However, these generated samples could bring more noise to the dataset [184] or complicate the work of the classifier by creating boundary samples [185]. In order to overcome these disadvantages, the ENN technique is used, which removes samples from both classes [186]. The ENN algorithm can be described as a data cleaning method, which may remove any sample whose class label is different from the class of two or more of its closest neighbors [183].

- (b)

- SMOTE-TL is a hybrid technique, which combines SMOTE and the Tomek links (TL) techniques. The TL technique is used for the same reasons as ENN—to reduce SMOTE disadvantages. Unlike ENN, TL analyzes only two samples that are the nearest neighbors and belong to different classes [187]. If and are the samples of the majority and minority classes, then a Tomek link is a distance between the pair [188,189], assuming no other class that fulfills the requirements listed below:

For balancing techniques, whose nominal feature values had been changed to continuous, the feature-converting rule (Equation (15)) was applied to the nominal value. For example, the binary feature’s values, after applying the SMOTE technique, have changed to values ; thus, the feature converting rule has been used

4.6. Machine Learning Methods

The field of study known as machine learning (ML) pertains to the study of computer algorithms, specifically the automated learning process that is facilitated through experience [190].

For financial distress classification, several supervised machine learning methods were used, and the selection process was influenced by previous research [9].

- Boosting is a powerful ensemble learning technique that transforms a group of learners from weak learners into strong learners by minimizing training errors [9]. The training process goes sequentially by reweighting and modifying current weights based on how accurately the previous learners predicted these samples [191]. In this study, categorical boosting (CatBoost) and extreme gradient boosting machine (XGBoost) techniques were implemented.

- (a)

- CatBoost (categorical boosting) is a new gradient boosting technique that implements ordered boosting into processing of categorical features [192]. Gradient boosting has a prediction shift problem, which ordered boosting solves. CatBoost is a modification of gradient boosting that avoids target leakage, i.e., ordered boosting splits the training dataset so that the model could be trained on one subset of data, while residuals could be calculated on another. Moreover, the processing of categorical features replaces the original, categorical variables with one or more numerical values, which reduces the number of steps in data preprocessing [193].

- (b)

- XGBoost (extreme gradient boosting machine) is a fast learning algorithm that combines gradient descent and tree ensemble learning to solve classification and regression problems [140]. Its main idea is to make the target function as minimal as possible while employing the gradient descent method to produce new trees based on all previous trees [194].

- DT (decision tree) extracts decision rules from a dataset and represents it in a tree-like structure for solving classification and regression problems [195]. The DT algorithm CART (classification and regression tree), which uses the Gini coefficient for the internal/decision node splitting, was implemented. The decision tree is a nonparametric method, and hence a small change in the data can develop a new tree [9].

- LG (logistic regression) is a statistical method used for modeling relationships between dependent and independent features. Moreover, the logistic function is used to model binary () dependent variables [9,198]. Based on our previous research, the assumption of multicollinearity is fulfilled for the LR method, i.e., features from the balanced dataset, that are highly correlated with other features, are removed.

- NB (naive Bayes) is based on the statistical Bayes theorem. It describes the probability of a given class label, based on features that might be related to a particular class label [158].

- Neuron networks is a group of ML methods that represent information processing in the mathematical manner of biological systems [199].

- (a)

- ANN (artificial neural network) is a computational model interconnected with a layered structure that contains input, output, and one or more hidden layer [200]. The multi-layer perception (MLP) is a popular type of ANN, where a feed-forward manner is used to place nodes and layers. Several processing layers causes the nonlinear associations between inputs and outputs to be created [94]. The hidden structure of the neuron network has been marked I–III, which indicates the hidden layers between input and dense layers. After each layer (except a dense one), a drop-out layer is implemented which is excluded from the calculation of the hidden structure.

- (b)

- CNN (convolutional neural network) is a deep learning architecture, which has a direct learning process from data. It works well for a large number of labeled data. The CNN architecture consists of convolution, pooling, and fully connected layers. These layers are used for automatic and adoptive learning of features for the classification tasks [9]. The hidden structure is indicated the same as in ANN. However, this indication is only used for conv_1d and flat layers; input, drop out, max-pooling, and the dense layer are not included in the calculation of the structure of the hidden layers.

- (c)

- ELM (extreme learning machine) is a training algorithm for single hidden layer feedforward neural networks. A normal distribution is used to assign weights between the input and hidden layers, while the pseudo-inverse technique is used to learn the weights between the hidden and output layers [201]. Moreover, the main benefits of ELM are fast learning speed, ease of implementation, and less human intervention when compared to the standard neural networks [202]. ELM was implemented with numeric values of for the hidden neurons.

- Random forest (RF) is an ensemble technique that involves creating multiple decision trees using various subsets of samples from the original dataset. Each tree in the RF is generated from a bootstrap sample of the data. Numerous individual trees are created, which have a low correlation with one another. In addition, the majority of these trees’ votes decide the class’s label [123,203].

- SVM (support vector machine) seeks to separate the classes by identifying the optimal decision boundary in a high-dimensional feature space. The possibilities of decision boundaries depend on the used SVM kernel function [9,204]. For example, a linear kernel makes the assumption that the relationship between the features and the class is linear. Hence, it tries to separate the classes in a linear manner. More complex decision boundaries (curves, circles, etc.) can be found using non-linear kernels, such as polynomial or radial basis functions. All these types of SVM kernel functions have been used in this research.

4.7. Evaluation Metrics

Evaluation metrics are determined based on the confusion matrix (see Table 9). In this research, non-financial distress enterprises are assigned to the positive class () and financial distress enterprises are assigned to the negative class (). In Table 9, denotes the number of true positives, is the number of true negatives, is the number of false positives, is the number of false negatives, is the number of actual positives, is the number of predicted positives, is the number of actual negatives, is the number of predicted negatives, and N is the number of all instances [165].

The most commonly used evaluation metrics, that are provided in Equations (16)–(23), were chosen for this research [9]. Moreover, higher values indicate a better performance for all these evaluation metrics.

- Precision—the ratio of true positives () to predicted positives ()

- Recall—the ratio of the true positives () to actual positives (), also known as sensitivity or (true positive ratio)

- Specificity—the ratio of the true negatives () to the actual negatives (). Also known as (true negative ratio)

- The area under the ROC curve (AUC)—a measure of how well a model can distinguish between two classes and is expressed as follows:where false positive ratio = 1—specificity.

- The is a metric that indicates the model’s discriminatory power. It is used as an alternative to AUC and usually used more often in the context of bankruptcy prediction. Moreover, the simple expression of is:

- Accuracy ()—the proportion of correctly classified instances

- F- is the harmonic mean of precision and recall, where the most common value of is 1. Therefore, the estimate is often called or -

- The G- is a geometric mean of the true positive rate and the true negative rate.

5. Results

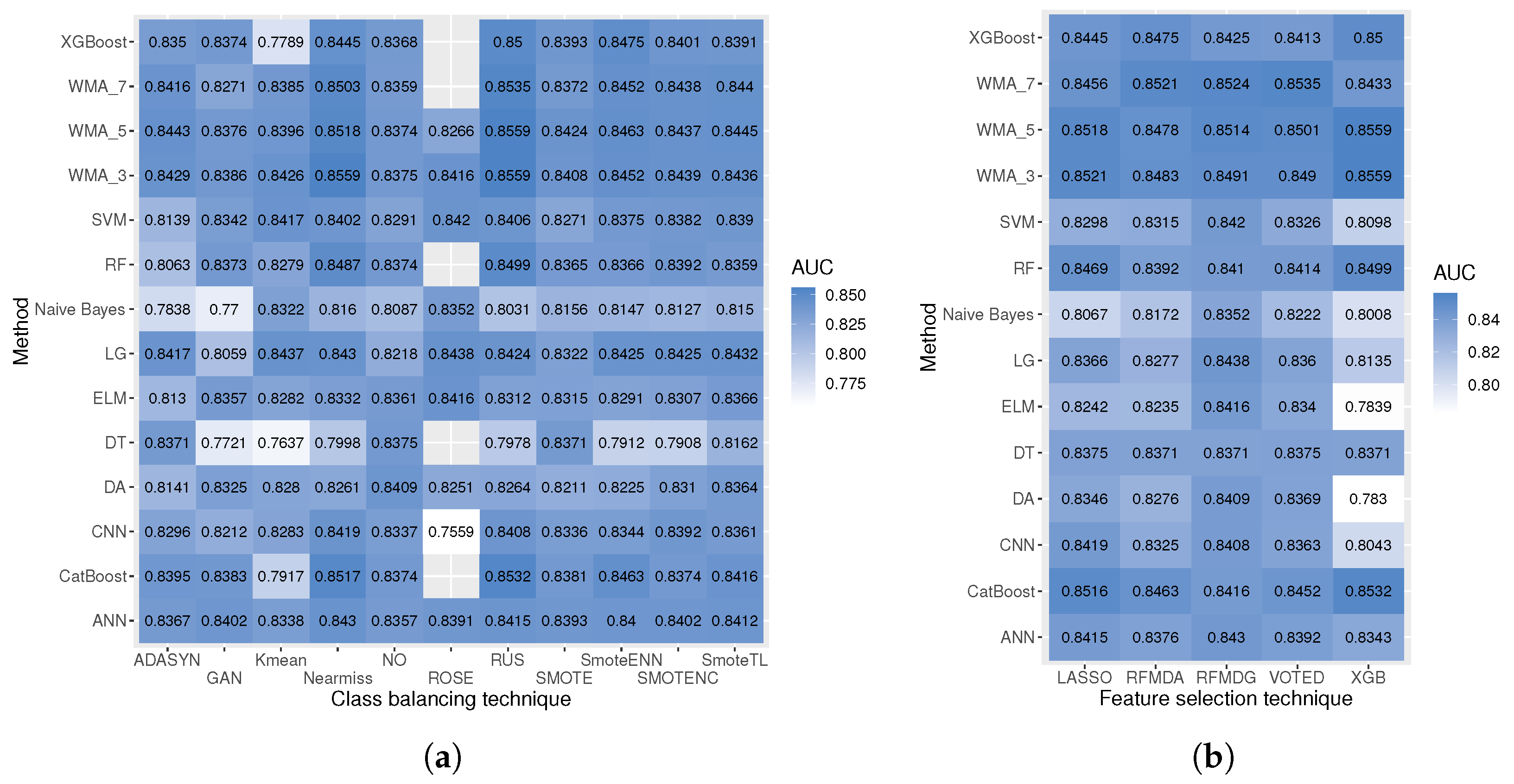

This experimental study examines the impact of diverse financial distress class definitions (determinations) in conjunction with balancing techniques to construct an efficient financial distress detection model. The experimental results involve five feature selection techniques, using 5 different number of feature set combinations, 10 different balancing techniques, 11 different machine learning models, and 14 different weighted majority algorithm combinations. In total, 9428 experiments have been conducted for the test dataset. The test sample had been separated from the training sample and included the last year’s (2022) data. Additionally, balancing techniques for the training sample have not been applied (see Figure 4). Thus, providing relevance to the current SMEs financial distress situation. To evaluate the efficiency of the model, the effectiveness criteria have been implemented. These criteria require that half of the good classification from both classes is present. However, as the test dataset is unbalanced, these halves are ≥ financial distress cases, and ≥20,600 non-financial distress cases. If this criterion is not filled, the outcome of the experiment is not further analyzed. This requirement has reduced the number of total experiments by approximately , resulting in experiments. Table 10 shows the best models based on the AUC metric. This metric was selected as the main metric for analysis since it can balance expressions for both classes. Also, additional evaluation metrics are provided to make this research more easily comparable with others. The best AUC score () is achieved using XGBoost feature selection technique with experimental max number strategy, Nearmiss, or RUS undersampling methods, and WMA_3.1 weighted majority algorithm (i.e., with CatBoost, XGBoost, and RF have equal voting weights). Moreover, Catboost has achieved the best result (), when analyzing algorithms individually. In the methodology part, five research questions were raised. The answers to each research question are presented in separate research parts, which are set out below.

5.1. Financial Distress Conditions Analysis