Assessing Consumer Implications of Reduced Salmon Supply and Environmental Impact in North America

, ,

, ,

Abstract

:1. Introduction

2. Literature Review

3. Methodology and Data

3.1. Machine Learning in Salmon Price Prediction

3.2. Data

4. Results and Discussion

4.1. Global Atlantic Salmon Production and Canada Share

4.2. Retail Price of Salmon

4.3. Market Distribution

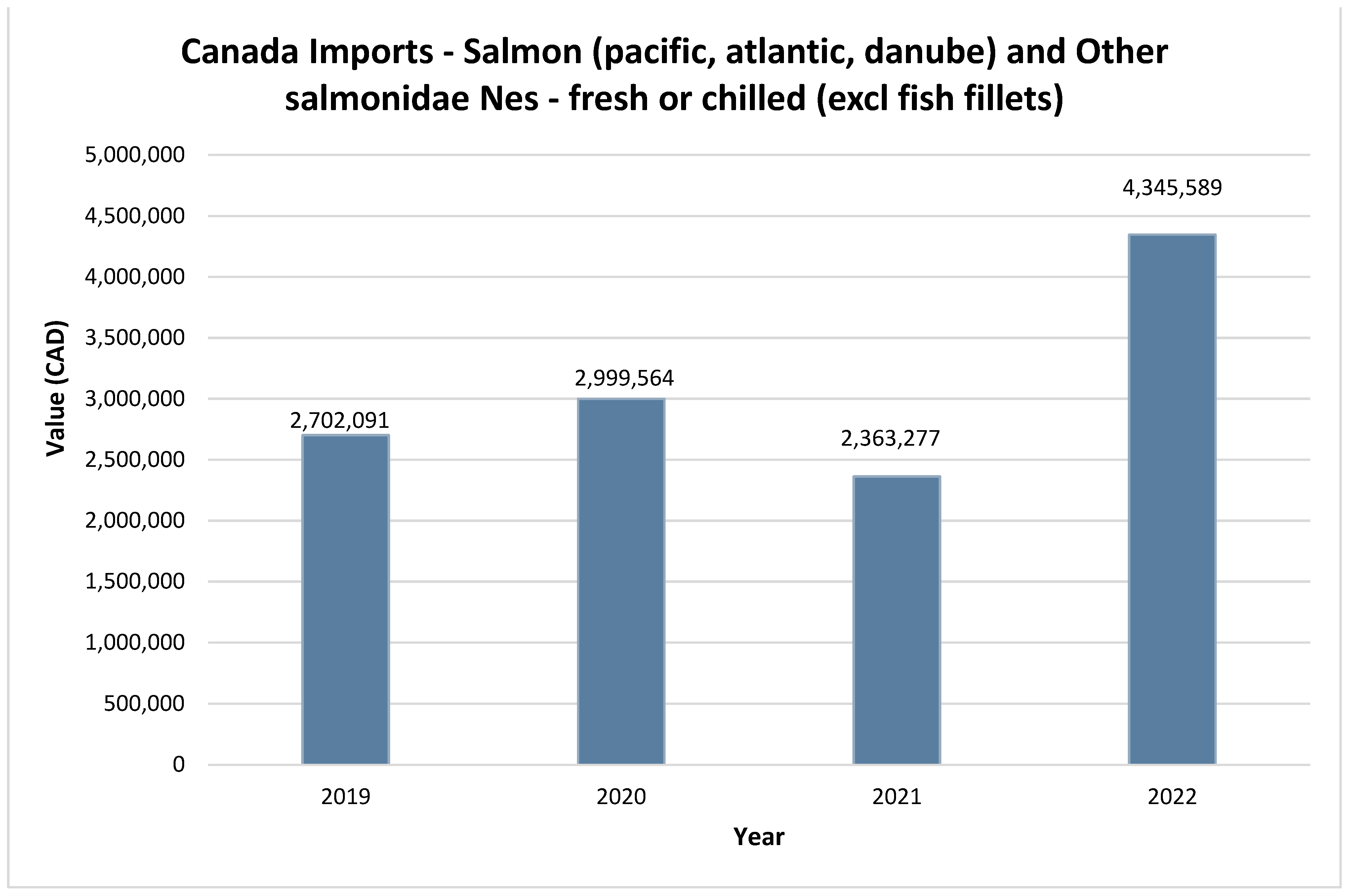

4.4. Market Shares of Salmon (Imports)—Canada

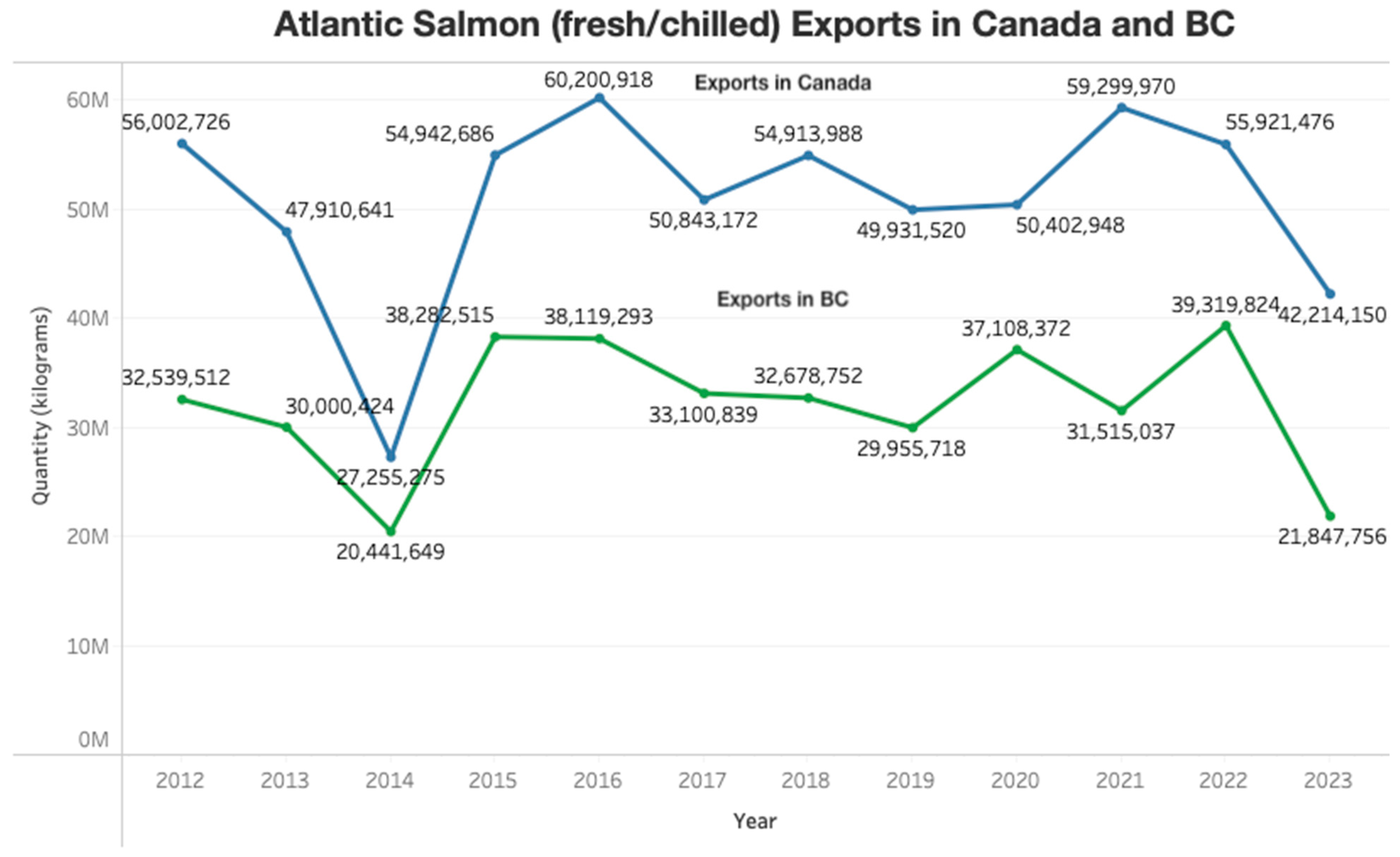

4.5. Farmed Atlantic Salmon Supply in Canada and BC

4.6. Canadian Farmed Atlantic Salmon Supply, World versus USA

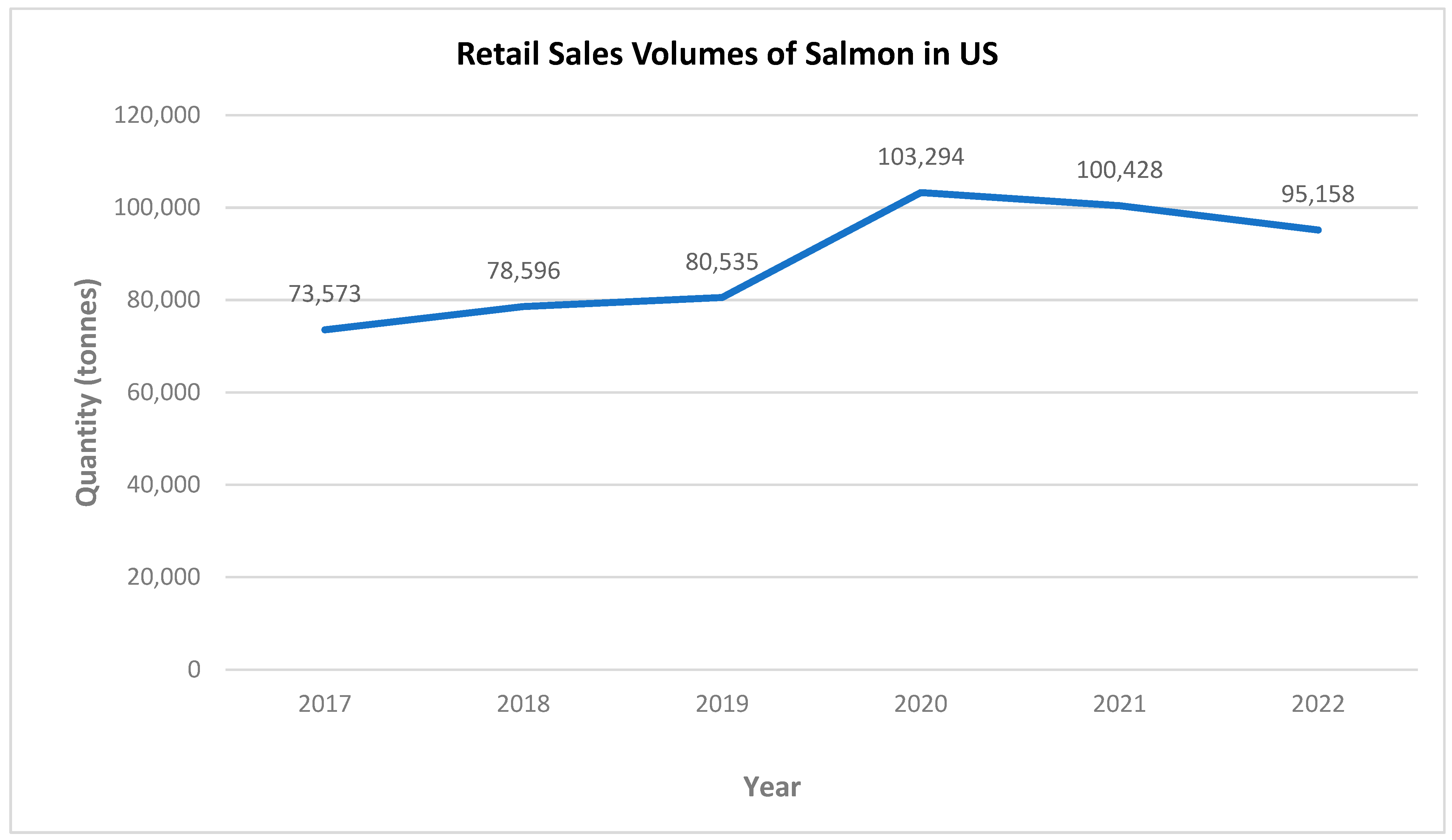

4.7. Salmon Sales and Consumer Demand

4.8. Seafood Consumption in Canada

4.9. Canadian Average Eating per Capita of Fish/Seafood

5. Forecasting

5.1. Forecasting the Monthly Average Retail Price of Salmon up to 2026

5.2. Carbon Footprint

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Date | Forecasted Price | Date | Forecasted Price | Date | Forecasted Price |

|---|---|---|---|---|---|

| 24 January | 29.06 | 25 January | 29.65 | 26 January | 30.23 |

| 24 February | 28.67 | 25 February | 29.25 | 26 February | 29.84 |

| 24 March | 29.12 | 25 March | 29.71 | 26 March | 30.29 |

| 24 April | 28.6 | 25 April | 29.18 | 26 April | 29.77 |

| 24 May | 29.76 | 25 May | 30.34 | 26 May | 30.92 |

| 24 June | 29.43 | 25 June | 30.01 | 26 June | 30.59 |

| 24 July | 28.79 | 25 July | 29.37 | 26 July | 29.96 |

| 24 August | 27.86 | 25 August | 28.44 | 26 August | 29.02 |

| 24 September | 28.5 | 25 September | 29.08 | 26 September | 29.66 |

| 24 October | 27.05 | 25 October | 27.64 | 26 October | 28.22 |

| 24 November | 28.41 | 25 November | 28.99 | 26 November | 29.58 |

| 24 December | 27.23 | 25 December | 27.82 | 26 December | 28.4 |

| Variable | Coefficient | z-Statistics |

|---|---|---|

| AR(1) | −0.445 *** (0.136) | −3.264 |

| MA.S(12) | −1.000 (1166.307) | −0.001 |

| σ2 | 0.897 (1046.328) | 0.001 |

| AIC | 158.842 | |

| BIC | 164.637 | |

| Jarque-Bera | 1.180 |

| Country | 2020 | 2021 | 2022 | 2023 (Until August) |

|---|---|---|---|---|

| USA | 38,302,333 | 49,327,231 | 47,256,253 | 25,944,836 |

| Chile | 15,804,696 | 16,434,882 | 15,522,162 | 13,655,955 |

| Norway | 2,244,782 | 3,837,213 | 4,610,537 | 2,931,071 |

| China | 3,912,098 | 3,287,334 | 3,745,725 | 2,126,420 |

| Mexico | 555,861 | 5,201,595 | 7,480,236 | 5,898,253 |

| Iceland | 251,567 | 777,498 | 1,828,093 | 732,743 |

| United Kingdom | 359,778 | 882,171 | 917,462 | 433,171 |

| Lithuania | 450,538 | 614,487 | 689,109 | 249,751 |

| Thailand | 1,369,993 | 1,649,477 | 1,018,263 | 495,149 |

| Poland | 615,508 | 806,309 | 385,082 | 144,016 |

| New Zealand | 151,218 | 469,326 | 108,543 | 87,521 |

| Netherlands | 172,603 | 98,559 | 91,274 | 65,690 |

| Sweden | 31,557 | 36,661 | 58,255 | 62,695 |

| Italy | 859 | 52,967 | 67,904 | 31,685 |

| Türkiye | 0 | 776 | 18,038 | 89,910 |

| Denmark | 67,101 | 108,581 | 261,189 | 113,595 |

| Canada | 213,181 | 161,847 | 230,967 | 62,330 |

| Ireland | 172,542 | 35,571 | 5938 | 14,181 |

| France | 74,746 | 1983 | 177 | 94,369 |

| Faroe Islands | 19,123 | 28,843 | 61,351 | 11,915 |

| Panama | 332,051 | 490,781 | 740,358 | 51,325 |

| Colombia | 3374 | 13,858 | 56,392 | 4064 |

| Japan | 108,280 | 19,151 | 8166 | 4492 |

| Brazil | 0 | 0 | 6357 | 4240 |

| Trinidad and Tobago | 0 | 8848 | 83,188 | 3026 |

| Viet Nam | 19 | 12,415 | 18,419 | 1145 |

| Sri Lanka | 0 | 0 | 284 | 4417 |

| Iran | 45 | 134 | 89 | 1655 |

| Germany | 9527 | 3681 | 38,338 | 1170 |

| Guyana | 0 | 0 | 944 | 1350 |

| Portugal | 1053 | 5030 | 1229 | 844 |

| Morocco | 0 | 200,016 | 0 | 16 |

| Australia | 0 | 2 | 125 | 5 |

| Benin | 0 | 0 | 0 | 2 |

| Korea, South | 0 | 112 | 0 | 0 |

| Argentina | 237,345 | 481,388 | 468,932 | 0 |

| Bangladesh | 0 | 0 | 0 | 0 |

| Belarus | 112 | 428 | 0 | 0 |

| Cameroon | 0 | 47 | 0 | 0 |

| Costa Rica | 0 | 0 | 191 | 0 |

| Ecuador | 4082 | 1067 | 727 | 0 |

| Egypt | 0 | 1 | 0 | 0 |

| Finland | 0 | 2 | 0 | 0 |

| Ghana | 0 | 902 | 0 | 0 |

| Greenland | 0 | 453 | 0 | 0 |

| Honduras | 0 | 11,610 | 1315 | 0 |

| Hong Kong | 0 | 2 | 0 | 0 |

| India | 0 | 0 | 0 | 0 |

| Indonesia | 44,089 | 20,583 | 226 | 0 |

| Israel | 349 | 10 | 0 | 0 |

| Kenya | 0 | 0 | 0 | 0 |

| Latvia | 3656 | 13,676 | 27,287 | 0 |

| Mauritania | 435 | 100,000 | 35 | 0 |

| Mozambique | 0 | 0 | 0 | 0 |

| Nigeria | 20 | 37 | 1 | 0 |

| Peru | 1588 | 111,903 | 30,566 | 0 |

| Philippines | 0 | 0 | 1688 | 0 |

| Russian Federation | 874,604 | 969,688 | 539,149 | 0 |

| Saudi Arabia | 0 | 0 | 0 | 0 |

| Senegal | 1 | 0 | 18 | 0 |

| Singapore | 3 | 0 | 0 | 0 |

| Spain | 40,848 | 19,455 | 542 | 0 |

| Switzerland | 1334 | 0 | 4839 | 0 |

| Taiwan | 44 | 0 | 60 | 0 |

| United Republic of Tanzania | 0 | 635 | 0 | 0 |

| Togo | 12,318 | 0 | 9 | 0 |

| Tunisia | 0 | 0 | 210 | 0 |

| Ukraine | 0 | 1155 | 648 | 0 |

| Total imports Quantity | 66,445,261 | 86,300,381 | 86,386,890 | 53,323,007 |

References

- Government of British Colombia. Salmon Aquaculture in British Colombia. Available online: https://www2.gov.bc.ca/assets/gov/environment/natural-resource-stewardship/environmental-assessments/eao-project-reviews/salmon-aquaculture-summary-report.pdf (accessed on 16 October 2023).

- Government of Canada. Farmed Salmon. Species Farmed in Canada. Available online: https://www.dfo-mpo.gc.ca/aquaculture/sector-secteur/species-especes/salmon-saumon-eng.htm (accessed on 16 October 2023).

- Cohen, B.I. Cohen Commission of Inquiry into the Decline of Sockeye Salmon in the Fraser River—Final Report. 2012. Available online: https://publications.gc.ca/site/eng/432516/publication.html (accessed on 20 October 2023).

- Saksida, S.M.; Greba, L.; Morrison, D.; Revie, C.W. Sea Lice on Wild Juvenile Pacific Salmon and Farmed Atlantic Salmon in the Northernmost Salmon Farming Region of British Columbia. Aquaculture 2011, 320, 193–198. [Google Scholar] [CrossRef]

- Jiménez, R.Á.; British Columbia Announces next Step in Transitioning from Open-Net Pen Aquaculture. Weare Aquaculture. 2022. Available online: https://weareaquaculture.com/news/22902 (accessed on 16 October 2023).

- RIAS Inc. Consequences of the Decision to Shut down Salmon Farming in the Discovery Islands; RIAS Inc.: Framingham, MA, USA, 2021. [Google Scholar]

- Fish Farming Expert. Dismay as Canadian Government Refuses to Reinstate BC Salmon Farm Licences. 2023. Available online: https://www.fishfarmingexpert.com/bernadette-jordan-british-columbia-discovery-islands/dismay-as-canadian-government-refuses-to-reinstate-bc-salmon-farm-licences/1490793#:~:text=TheDecember2020decisionto,healthysalmon%2CsaidtheBCSFA (accessed on 17 October 2023).

- Pauly, D.; Zeller, D. Catch Reconstructions Reveal That Global Marine Fisheries Catches Are Higher than Reported and Declining. Nat. Commun. 2016, 7, 10244. [Google Scholar] [CrossRef]

- Hognes, E.S.; Ziegler, F.; Sund, V. Carbon Footprint and Area Use of Farmed Norwegian Salmon; SINTEF: Oslo, Norway, 2011. [Google Scholar]

- Farmery, A.K.; Gardner, C.; Green, B.S.; Jennings, S.; Watson, R.A. Domestic or Imported? An Assessment of Carbon Footprints and Sustainability of Seafood Consumed in Australia. Environ. Sci. Policy 2015, 54, 35–43. [Google Scholar] [CrossRef]

- Fisheries and Oceans Canada. Canada Fish and Seafood Trade. Available online: https://www.dfo-mpo.gc.ca/ea-ae/economic-analysis/Canada-Fish-Seafood-trade-commerce-poisson-fruits-de-mer-eng.html (accessed on 23 October 2023).

- The Globe and Mail. New Fisheries Minister Wades into Bitter Row over Closing of Salmon Farms. 2023. Available online: https://www.theglobeandmail.com/politics/article-new-fisheries-minister-wades-into-bitter-row-over-closing-of-salmon/ (accessed on 23 October 2023).

- Logan, C. Tale of Two Coasts: How Canada’s Approach to Salmon Farming Differs from East to West. National Observer. 2023. Available online: https://www.nationalobserver.com/2023/10/10/tale-two-coasts-how-canadas-approach-salmon-farming-differs-east-west (accessed on 16 October 2023).

- FAO. The State of Food Insecurity in the World 2014: Strengthening the Enabling Enviroment for Food Security and Nutrition; FAO: Rome, Italy, 2014. Available online: https://www.fao.org/3/i4030e/i4030e.pdf (accessed on 20 October 2023).

- Grafton, R.Q.; Williams, J.; Jiang, Q. Food and Water Gaps to 2050: Preliminary Results from the Global Food and Water System (GFWS) Platform. Food Secur. 2015, 7, 209–220. [Google Scholar] [CrossRef]

- Tilman, D.; Balzer, C.; Hill, J.; Befort, B.L. Global Food Demand and the Sustainable Intensification of Agriculture. Proc. Natl. Acad. Sci. USA 2011, 108, 20260–20264. [Google Scholar] [CrossRef]

- Ahmed, N.; Thompson, S.; Turchini, G.M. Organic Aquaculture Productivity, Environmental Sustainability, and Food Security: Insights from Organic Agriculture. Food Secur. 2020, 12, 1253–1267. [Google Scholar] [CrossRef]

- FAO. The State of World Fisheries and Aquaculture 2020; FAO: Rome, Italy, 2020. [Google Scholar] [CrossRef]

- Gephart, J.A.; Henriksson, P.J.G.; Parker, R.W.R.; Shepon, A.; Gorospe, K.D.; Bergman, K.; Eshel, G.; Golden, C.D.; Halpern, B.S.; Hornborg, S.; et al. Environmental Performance of Blue Foods. Nature 2021, 597, 360–365. [Google Scholar] [CrossRef]

- Garlock, T.; Asche, F.; Anderson, J.; Bjørndal, T.; Kumar, G.; Lorenzen, K.; Ropicki, A.; Smith, M.D.; Tveterås, R. A Global Blue Revolution: Aquaculture Growth Across Regions, Species, and Countries. Rev. Fish. Sci. Aquac. 2020, 28, 107–116. [Google Scholar] [CrossRef]

- Hilborn, R.; Banobi, J.; Hall, S.J.; Pucylowski, T.; Walsworth, T.E. The Environmental Cost of Animal Source Foods. Front. Ecol. Environ. 2018, 16, 329–335. [Google Scholar] [CrossRef]

- Froehlich, H.E.; Runge, C.A.; Gentry, R.R.; Gaines, S.D.; Halpern, B.S. Comparative Terrestrial Feed and Land Use of an Aquaculture-Dominant World. Proc. Natl. Acad. Sci. USA 2018, 115, 5295–5300. [Google Scholar] [CrossRef] [PubMed]

- MacLeod, M.J.; Hasan, M.R.; Robb, D.H.F.; Mamun-Ur-Rashid, M. Quantifying Greenhouse Gas Emissions from Global Aquaculture. Sci. Rep. 2020, 10, 11679. [Google Scholar] [CrossRef]

- Golden, C.D.; Koehn, J.Z.; Shepon, A.; Passarelli, S.; Free, C.M.; Viana, D.F.; Matthey, H.; Eurich, J.G.; Gephart, J.A.; Fluet-Chouinard, E.; et al. Aquatic Foods to Nourish Nations. Nature 2021, 598, 315–320. [Google Scholar] [CrossRef]

- Sharif, M.; Zafar, M.H.; Aqib, A.I.; Saeed, M.; Farag, M.R.; Alagawany, M. Single Cell Protein: Sources, Mechanism of Production, Nutritional Value and Its Uses in Aquaculture Nutrition. Aquaculture 2021, 531, 735885. [Google Scholar] [CrossRef]

- Dawood, M.A.O.; Koshio, S. Application of Fermentation Strategy in Aquafeed for Sustainable Aquaculture. Rev. Aquac. 2020, 12, 987–1002. [Google Scholar] [CrossRef]

- Smith, M.D.; Roheim, C.A.; Crowder, L.B.; Halpern, B.S.; Turnipseed, M.; Anderson, J.L.; Asche, F.; Bourillón, L.; Guttormsen, A.G.; Khan, A.; et al. Sustainability and Global Seafood. Science 2010, 327, 784–786. [Google Scholar] [CrossRef]

- Hua, K.; Cobcroft, J.M.; Cole, A.; Condon, K.; Jerry, D.R.; Mangott, A.; Praeger, C.; Vucko, M.J.; Zeng, C.; Zenger, K.; et al. The Future of Aquatic Protein: Implications for Protein Sources in Aquaculture Diets. One Earth 2019, 1, 316–329. [Google Scholar] [CrossRef]

- Filipski, M.; Belton, B. Give a Man a Fishpond: Modeling the Impacts of Aquaculture in the Rural Economy. World Dev. 2018, 110, 205–223. [Google Scholar] [CrossRef]

- FAO. The State of World Fisheries and Aquaculture: Contributing to Food Security and Nutrition for All; FAO: Rome, Italy, 2016; Available online: https://www.fao.org/3/i5555e/i5555e.pdf (accessed on 20 October 2023).

- Anderson, J.L.; Asche, F.; Garlock, T.; Chu, J. Aquaculture: Its Role in the Future of Food. In World Agricultural Resources and Food Security; Emerald Publishing Limited: Bingley, UK, 2017; pp. 159–173. [Google Scholar] [CrossRef]

- Fisheries and Oceans Canada. Outlook to 2027 for Canadian Fish and Seafood. 2018. Available online: https://waves-vagues.dfo-mpo.gc.ca/library-bibliotheque/40732836.pdf (accessed on 16 October 2023).

- Government of Canada. Pacific Aquaculture Transition—What We Heard Report Phases 1 and 2; Government of Canada: Ottawa, ON, Canada, 2023.

- Nourish Food Marketing. Canadian Consumption of Seafood; Nourish Food Marketing: Toronto, ON, Canada, 2022. [Google Scholar]

- Tsoumakas, G. A Survey of Machine Learning Techniques for Food Sales Prediction. Artif. Intell. Rev. 2019, 52, 441–447. [Google Scholar] [CrossRef]

- Landwehr, N.; Hall, M.; Frank, E. Logistic Model Trees. Mach. Learn. 2005, 59, 161–205. [Google Scholar] [CrossRef]

- Bloznelis, D. Short-term Salmon Price Forecasting. J. Forecast. 2018, 37, 151–169. [Google Scholar] [CrossRef]

- Gladju, J.; Kamalam, B.S.; Kanagaraj, A. Applications of Data Mining and Machine Learning Framework in Aquaculture and Fisheries: A Review. Smart Agric. Technol. 2022, 2, 100061. [Google Scholar] [CrossRef]

- Hwang, Y. Data-Driven Agricultural Market Prediction. 2019. Available online: https://s-space.snu.ac.kr/bitstream/10371/150949/1/000000154117.pdf (accessed on 18 October 2023).

- Bjørnstad, H.; Halvorsen, Ø.L.; Rognås, V.C.J. Forecasting the Price of Salmon Using Machine Learning Algorithms, Norwegian University of Science and Technology. 2023. Available online: https://ntnuopen.ntnu.no/ntnu-xmlui/handle/11250/3071433?locale-attribute=en (accessed on 20 October 2023).

- McHugh, C.; Coleman, S.; Kerr, D.; McGlynn, D. Forecasting Day-Ahead Electricity Prices with A SARIMAX Model. In Proceedings of the 2019 IEEE Symposium Series on Computational Intelligence (SSCI), Xiamen, China, 6–9 December 2019; IEEE: New York, NY, USA, 2019; pp. 1523–1529. [Google Scholar] [CrossRef]

- Statistics Canada. Monthly Average Retail Prices for Selected Products, Table: 18-10-0245-01. Available online: https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1810024501 (accessed on 17 October 2023).

- British Columbia Government. Sector Snapshot 2019: B.C. Seafood. 2020. Available online: https://www2.gov.bc.ca/assets/gov/farming-natural-resources-and-industry/agriculture-and-seafood/statistics/industry-and-sector-profiles/sector-snapshots/sector_snapshot_2019_-_seafood.pdf (accessed on 21 October 2023).

- Fisheries and Oceans Canada. Aquaculture in British Columbia. Available online: https://www.pac.dfo-mpo.gc.ca/aquaculture/index-eng.html (accessed on 23 October 2023).

- Kontali. Global Salmon Production and Market Update: Systemizing the World of Aquaculture and Fisheries. 2023. Available online: https://edge.kontali.com/ (accessed on 23 October 2023).

- Statistics Canada. Aquaculture, Production and Value; Statistics Canada: Ottawa, ON, Canada, 2023. [CrossRef]

- Valdés, A. Net Food-Importing Developing Countries: Who They Are, and Policy Options for Global Price Volatility. 2012. Available online: https://www.files.ethz.ch/isn/152811/net-food-importing-developing-countries-who-they-are-and-policy-options-for-global-price-volatility.pdf (accessed on 16 October 2023).

- Gouel, C. Trade Policy Coordination and Food Price Volatility. Am. J. Agric. Econ. 2016, 98, 1018–1037. [Google Scholar] [CrossRef]

- Nielsen. Retail Trend of Atlantic Salmon: Retail Scan Numbers for Seafood in the US; Nielsen: New York, NY, USA, 2023. [Google Scholar]

- Charlebois, S.; Colombo, S. Canadians Cast Their Nets of Preference: New Study Reveals Insights into Seafood Choices and Sustainability. Agri. Food, 2023; Unpublished. [Google Scholar]

- Osmond, A.T.Y.; Charlebois, S.; Colombo, S.M. Exploratory Analysis on Canadian Consumer Perceptions, Habits, and Opinions on Salmon Consumption and Production in Canada. Aquac. Int. 2023, 31, 179–193. [Google Scholar] [CrossRef]

- RIAS Inc. Economic And Financial Impacts of Minister Murray’s Transition Plan for BC Salmon Farms; RIAS Inc.: Ottawa, ON, Canada, 2023. [Google Scholar]

| Year | Global Atlantic Salmon Production | North America Harvest Quantity | Canada Share | USA Share | BC Share |

|---|---|---|---|---|---|

| 2019 | 2,577,900 | 158,300 | 137,500 | 20,800 | 81,500 |

| 2020 | 2,712,600 | 156,800 | 136,800 | 20,000 | 87,000 |

| 2021 | 2,896,000 | 161,000 | 142,000 | 19,000 | 79,000 |

| 2022 | 2,865,700 | 151,000 | 131,500 | 19,500 | 81,500 |

| 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|

| Chicken | 29.5% | 30.7% | 30.3% | 30.8% |

| Beef | 12.6% | 13.2% | 13.0% | 12.2% |

| Fish/Fish Dishes | 8.5% | 7.9% | 8.5% | 7.9% |

| Pork | 6.2% | 6.5% | 6.5% | 6.3% |

| Turkey | 1.7% | 1.6% | 1.4% | 1.2% |

| All other Meat | 6.1% | 6.7% | 6.2% | 6.7% |

| Other Protein (meat alternative) | 35.4% | 33.4% | 34.1% | 34.9% |

| 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|

| Meat Protein | 585 | 569 | 586 | 575 |

| Fish/Seafood | 61 | 56 | 62 | 54 |

| Fish/Fish Dishes | 44 | 42 | 45 | 40 |

| Salmon Fillet/Steaks | 13 | 12 | 13 | 11 |

| Seafood/Seafood Dishes | 17 | 14 | 17 | 14 |

| Salmon Supplier | Distance from Border to the Border (km) | Kg CO2—eq/Tonne km | Estimated in Million Tonnes CO2 Emissions km (2020) | Estimated in Million Tonnes CO2 Emissions km (2021) | Estimated in Million Tonnes CO2 Emissions km (2022) | Estimated in Million Tonnes CO2 Emissions km (Until August 2023) |

|---|---|---|---|---|---|---|

| Norway | 1190 | 702.5 | 1.577 | 2.6956 | 3.2389 | 2.0591 |

| UK | 2849 | 1681.8 | 0.605 | 1.4836 | 1.543 | 0.7285 |

| Chile | 6686 | 3946.8 | 62.378 | 64.8652 | 61.263 | 53.8973 |

| China | 4745 | 2800.98 | 10.9577 | 9.2078 | 10.4917 | 5.9561 |

| Mexico | 1808 | 1067.27 | 0.5933 | 5.5515 | 7.9834 | 6.295 |

| Iceland | 1647 | 972.23 | 0.2446 | 0.7559 | 1.7773 | 0.7124 |

| Total CO2 emissions Produced | 76.3556 | 84.5596 | 86.2973 | 69.6484 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Charlebois, S.; Gone, K.P.; Saxena, S.; Colombo, S.; Sarker, B. Assessing Consumer Implications of Reduced Salmon Supply and Environmental Impact in North America. Sustainability 2024, 16, 3629. https://0-doi-org.brum.beds.ac.uk/10.3390/su16093629

Charlebois S, Gone KP, Saxena S, Colombo S, Sarker B. Assessing Consumer Implications of Reduced Salmon Supply and Environmental Impact in North America. Sustainability. 2024; 16(9):3629. https://0-doi-org.brum.beds.ac.uk/10.3390/su16093629

Chicago/Turabian StyleCharlebois, Sylvain, Keshava Pallavi Gone, Swati Saxena, Stefanie Colombo, and Bibhuti Sarker. 2024. "Assessing Consumer Implications of Reduced Salmon Supply and Environmental Impact in North America" Sustainability 16, no. 9: 3629. https://0-doi-org.brum.beds.ac.uk/10.3390/su16093629